Aerial view of the Jiangyin Port City Economic Zone | Baidu, Feb 9, 2025

The Petrochemical Revolution: How Fujian Zhongjiang's Backward Integration Across the C3 Value Chain Exemplifies Strategic Transformation in Global Petrochemicals

The global petrochemical industry is undergoing a fundamental transformation as companies across the plastic conversion sector embark on unprecedented backward integration strategies, fundamentally reshaping the traditional boundaries between refining, chemicals production, and downstream processing. This strategic shift represents more than incremental expansion; it signals a complete reimagining of how value chains operate in an era of supply chain volatility, margin compression, and the relentless pursuit of operational efficiency.

The Economics of Scale and Integration

The modern petrochemical landscape has become defined by the economics of mega-scale operations, where companies are discovering that vertical integration offers compelling advantages over traditional market-based transactions. Already, more than 30% of the world's refineries are now integrated with commodity petrochemicals, creating sites that benefit from both diversified product portfolios and enhanced operational synergies. This integration trend has been particularly pronounced in Asia, where approximately 70% of polypropylene plants by capacity are now integrated back to steam cracking or propane dehydrogenation sources of propylene.

Fuzhou Wanjing PDH3 began operation on May 15, 2025 | Shaanxi Chemical Construction, via oil.in-en.com

The financial rationale driving this integration is clear when examining the transaction cost economics that govern petrochemical operations. Companies are finding that the coordination efficiency gained through vertical integration significantly reduces the transaction costs associated with intermediary relationships, while simultaneously providing greater control over quality standards and supply chain reliability. The scale advantages are particularly evident in propane dehydrogenation operations, where single-unit capacities have expanded dramatically, with most recent facilities now reaching the impressive nameplate capacity of 900 thousand tonnes per year of propane.

China's Strategic Transformation and Global Implications

China's chemical industry expansion has become the defining force reshaping global petrochemical dynamics, with the country pursuing aggressive backward integration strategies that extend from plastic conversion all the way to crude oil refining. Chinese enterprises in the polyester value chain, including companies like Hengli, Shenghong, and Hengyi Petrochemical, have established massive refinery and integrated petrochemical complex projects that demonstrate the strategic imperative of securing upstream feedstock sources. This transformation is exemplified by companies that initially established themselves as textile manufacturers but have systematically integrated backward through purified terephthalic acid (PTA) production, paraxylene (PX) manufacturing, and ultimately into crude oil refining.

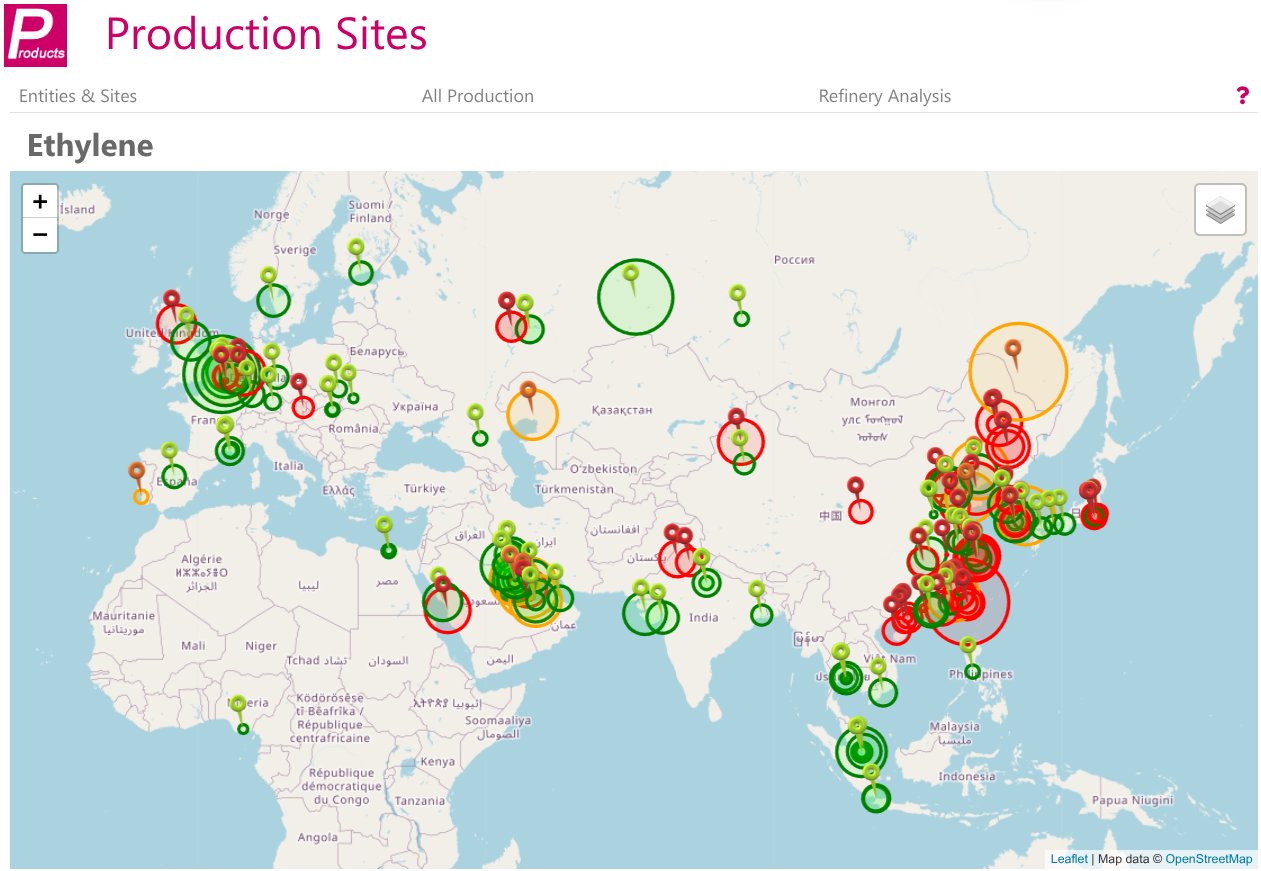

Ethylene production map centered on Eurasia | Source: portfolio planning PLUS

The scale of China's capacity expansion defies traditional market logic, with ethylene nameplate capacity increasing from approximately 26 million tonnes per year in 2019 to 54 million tonnes by 2024, more than doubling over the six-year period, with a further capacity increase expected to reach 66 million tonnes by 2025 according to industry estimates. China's ethylene and propylene capacity in 2025 is forecast to be 121% and 179% more than local demand respectively, creating structural oversupply that forces Chinese producers to seek international markets for their excess production. This capacity buildup has been facilitated by China's demonstrated ability to construct petrochemical facilities approximately 40% faster than international competitors, with paraxylene plants being completed in around 30 months compared to 48 months elsewhere, while also maintaining capital costs that are approximately 20% lower than the rest of Asia.

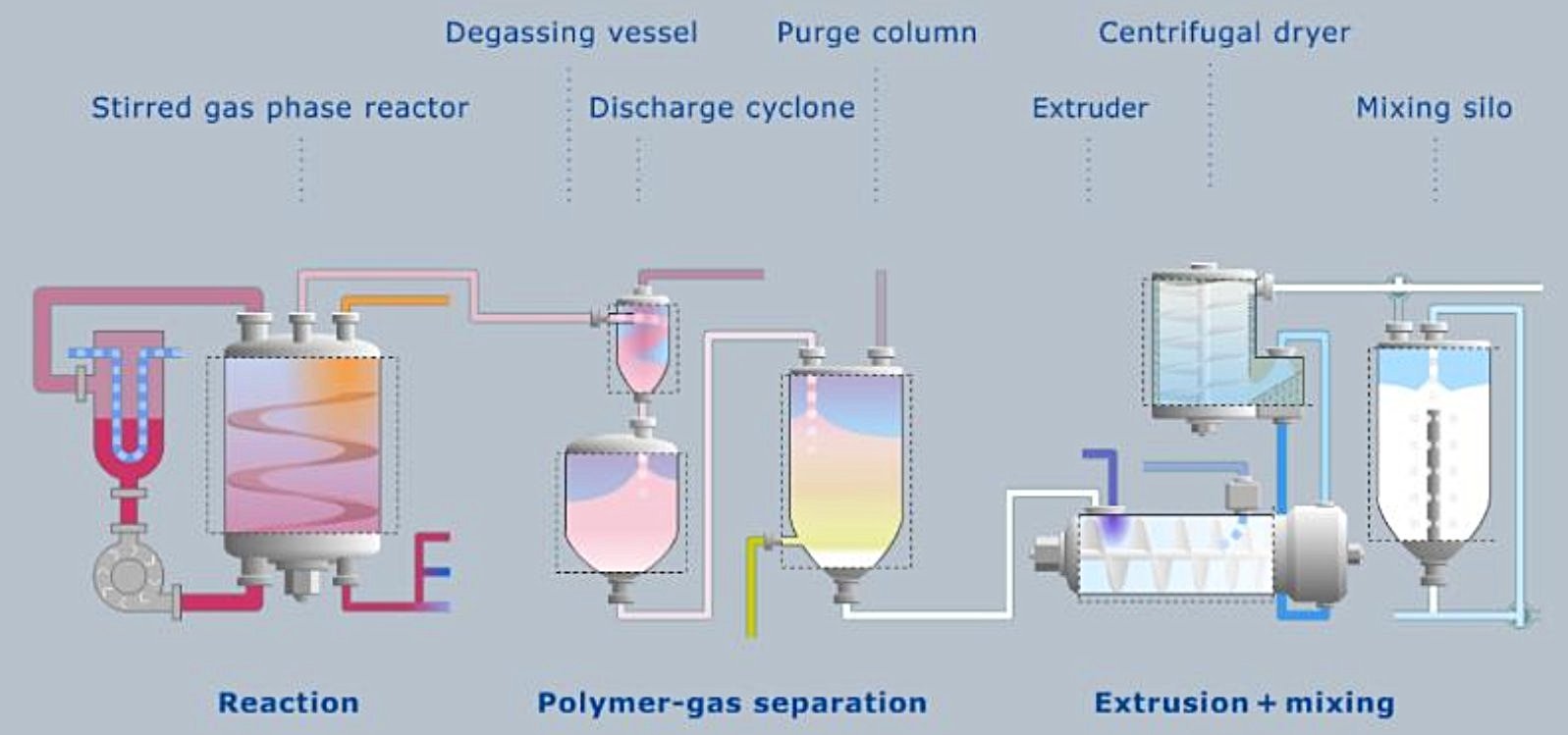

The Fujian Zhongjiang Model: From BOPP to Integrated Petrochemicals

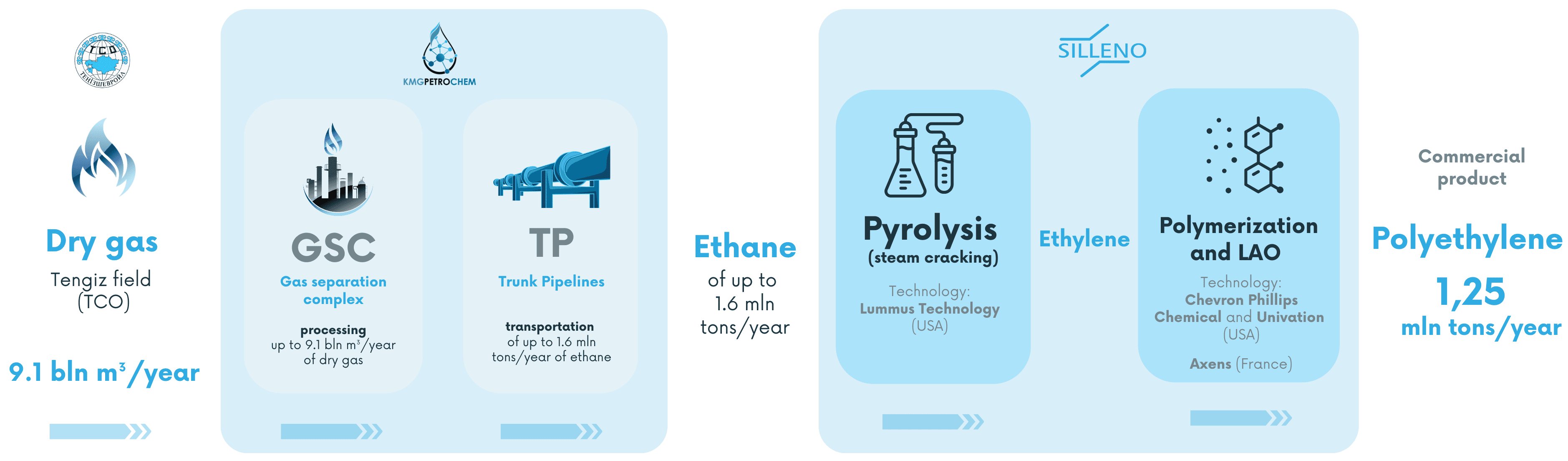

The evolution of Fujian Zhongjiang Petrochemicals Group represents a paradigmatic case study in strategic backward integration within the C3 value chain. The company's transformation from its origins as a biaxially oriented polypropylene film producer to a fully integrated propane-to-polypropylene operator demonstrates how specialized downstream companies can achieve remarkable operational synergies through systematic upstream expansion. Beginning as "the world's film king" in the BOPP sector, China Flexible Packaging Group recognized the vulnerability inherent in depending on volatile propylene markets and embarked on a methodical integration strategy that now spans from LPG import terminals through propane dehydrogenation to polypropylene production and finally to BOPP film manufacturing.

Fuzhou Propane Cryogenic Tank Storage | Seatao, May 29, 2023

This integration model has enabled the company to achieve unique operational advantages, including circular hydrogen utilization where byproduct hydrogen from propane dehydrogenation fuels adjacent chemical units, reducing operational costs by approximately 15%. The company's current integrated structure encompasses:

This level of integration allows the company to maintain 40% captive BOPP consumption while simultaneously supplying regional injection molding clusters, demonstrating how backward integration can create both supply security and market flexibility.

Technology and Process Innovation Driving Integration

The technological foundation enabling these massive integration projects has evolved significantly, with process innovations making large-scale operations both technically feasible and economically attractive. In polyethylene production, the latest advances exemplified by Univation's 800,000 tonnes per year UNIPOL PE Process and Chevron Phillips Chemical's MarTech single-loop slurry process deploying 1,000,000 tonnes per year HDPE lines demonstrate how reactor engineering and process optimization have redefined the limits of scale and flexibility. These technological advances are not merely incremental improvements but represent fundamental breakthroughs in managing the intense heat and mixing requirements of high-throughput polymerization while maintaining operational reliability and efficiency. Polypropylene production has witnessed comparable scale expansions, with Fujian Zhongjiang's integrated facilities demonstrating the progression from initial 500,000 tonnes per year production lines to the current world-scale 600,000 tonnes per year units utilizing LyondellBasell's Spheripol technology.

Fujian Meide Petrochemical Fuzhou complex - running Oleflex plant in the foreground, Catofin plant to be started up later in 2025 behind it | Baidu, Nov 2023

More dramatic scale increases are now seen at the origin of the C2 and C3 value chains. As we previously reported, ethane cracking facilities are now reaching ethylene production capacities of 2.1 million tonnes per year. The propane dehydrogenation sector is experiencing a similar technological evolution, with catalyst systems lying at the heart of process economics. The scale of PDH operations has now reached unprecedented levels, with individual units achieving 900,000 tonnes per year capacity, as demonstrated by Fujian Meide's facility that commenced operations in May 2025 and Fuzhou Wanjing's unit scheduled for startup later in 2025, both utilizing Lummus CATOFIN technology with specialized Clariant catalysts. Advanced PDH technologies now routinely operate at temperatures between 480-600°C under low pressure conditions, achieving propylene yields and selectivity that make large-scale operations economically viable even in regions with higher feedstock costs. The development of these technologies has been crucial in enabling companies to pursue backward integration strategies, as the improved economics of PDH operations make it feasible for downstream plastic producers to justify the substantial capital investments required for upstream expansion.

Strategic Implications and Future Trajectory

The acceleration of vertical integration in the petrochemical sector reflects broader strategic imperatives that extend beyond simple cost optimization. Companies are recognizing that integration provides critical protection against supply chain disruptions, market volatility, and competitive pressures that have intensified in recent years. The consolidation dynamics within different specialty chemical segments are driving companies to focus their portfolios while simultaneously optimizing their business models through strategic integration.

Zhongjing Petrochemical Group facilities in Jiangyin Industrial Zone | Chenhr

The implications of this integration trend extend to global trade patterns and competitive dynamics, as integrated producers gain significant advantages over standalone operations. The economic benefits of integration become particularly pronounced during market downturns, when integrated refinery-petrochemical sites consistently outperform their fuels-only peers due to their diversified revenue streams and operational flexibility. This performance differential is driving further consolidation as companies recognize that scale and integration have become essential requirements for long-term competitiveness in the evolving petrochemical landscape.

The future trajectory of the industry suggests that this integration trend will continue to accelerate, driven by the fundamental economics of large-scale operations and the strategic advantages of supply chain control. As companies like Fujian Zhongjiang demonstrate, successful integration requires not merely the ability to execute large capital projects, but the strategic vision to create synergistic value across the entire value chain while maintaining operational excellence at each stage of production. The companies that master this integration challenge will likely emerge as the dominant players in the next phase of global petrochemical industry evolution.

This article includes market data from WoodMckenzie, S&P Global, ICIS, Argus Media and other sources.

#refinerieintegration #backwardintegration #ethylene #propylene #valuechain #lyondellbasell #lummus #uop #honeywell #sinopec #technip

")