The Berre petrochemical plant is one of the sites involved in exclusive sales negotiations between LyondellBasell and Aequita | PHOTO: Frédéric SPEICH, La Provence

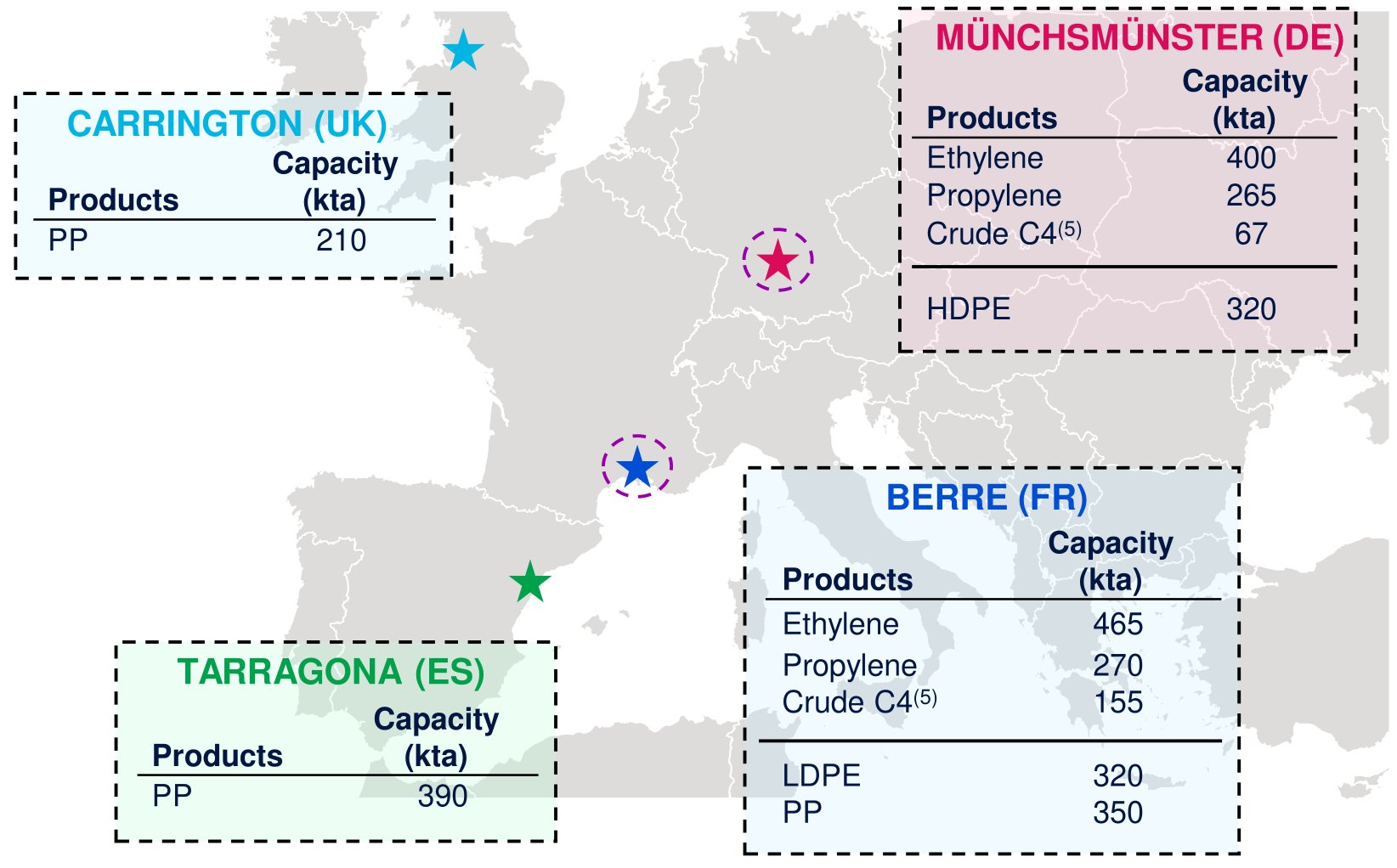

LyondellBasell’s (LYB) agreement to divest four major European production sites to AEQUITA marks a pivotal moment not only for the company but for the continent’s entire petrochemical sector. The transaction, encompassing plants in France (Berre), Germany (Münchsmünster), the UK (Carrington), and Spain (Tarragona), is emblematic of a broader industry shift as producers grapple with persistent overcapacity, high costs, and the need for structural transformation.

LyondellBasell Transaction Footprint | Jun 5, 2025 | LyondellBasell Investors Presentation

Strategic Rationale: From Rationalization to Refocus

LYB’s decision to sell these assets is rooted in a deliberate strategy to sharpen its operational focus and enhance profitability. The divested sites, which together account for roughly 1.4 million tonnes per year of polyolefins and olefins output, have delivered only modest returns while consuming significant capital—averaging €110 million in annual capex from 2020 to 2024. By transferring these facilities to AEQUITA, LYB expects to reduce its fixed costs by approximately €400 million per year and reallocate capital toward its most competitive and sustainable European operations.

Notably, this move is not an isolated event. LYB’s review initially spanned six sites, including Brindisi (Italy)—where one polypropylene plant has already been shuttered—and Maasvlakte (Netherlands), a joint venture (with Covestro) asset not included in the AEQUITA deal. This highlights the depth of LYB’s strategic review and underscores the scale of rationalization underway across the region.

Industry Context: A Wave of Closures and Consolidation

LYB’s asset sale is part of a much larger trend. European petrochemical producers are facing unprecedented headwinds: high energy costs, aging infrastructure, tightening environmental regulations, and lackluster demand. Other industry leaders, such as ExxonMobil, Sabic, and Indorama Ventures, have also closed or downsized European operations in the past year. Ultimately, up to half of the continent’s ethylene crackers could ultimately face closure, as the economics of small, old plants become increasingly untenable.

This rationalization wave is not simply a response to cyclical weakness but a recognition of structural change. Freight disruptions and temporary supply shocks have only delayed the inevitable need for consolidation and transformation.

LyondellBasell' Assets for Sale | Jun 5, 2025 | LyondellBasell Investors Presentation

Deal Structure and Financial Terms

The transaction with AEQUITA is structured to enable a smooth transition:

- LYB will contribute €265 million (of a €275 million carve-out support fund) to facilitate the separation, with AEQUITA providing €10 million.

- LYB stands to receive up to €100 million in earnouts over three years.

- AEQUITA will assume approximately €150 million in pension and employee liabilities, as well as all environmental obligations.

- The deal is expected to close in the first half of 2026, subject to regulatory and works council approvals.

Importantly, LYB’s exit from these sites will also spare it from the need to invest hundreds of millions in decarbonization upgrades, particularly at Berre and Münchsmünster, where meeting 2030 emissions targets would have required major capital outlays.

LYB’s European Commitment: Core Sites and Circular Ambitions

Despite the high-profile asset sale, LYB has made clear that Europe remains a core region. The company’s retained portfolio includes technologically advanced and economically advantaged sites in Ferrara, Frankfurt, Ludwigshafen, and Rotterdam, as well as integrated supply hubs in Cologne and specialty operations in APS. These facilities are positioned to support LYB’s ambitions in circular and low-carbon solutions, including advanced recycling (MoReTec) and the CirculenRecover product line.

LYB’s future European footprint will be more focused, with a higher share of capacity in cost-advantaged regions (U.S. and Middle East), rising from 61% to 68% post-transaction. The company is also stepping up investment in recycling and circular economy initiatives at its core sites, aiming to deliver 2 million tonnes per year of recycled and renewable polymers by 2030.

Market Implications and Competitive Dynamics

LYB’s withdrawal from these European assets will reshape the regional supply landscape, opening opportunities for Middle Eastern and Asian exporters to increase their market share. The move also contrasts with the strategies of some competitors, such as SABIC, which is expanding its footprint in Asia. For LYB, the divestment enables a sharper focus on direct customers, brand owners, and high-growth segments, while freeing up resources for innovation and portfolio upgrades.

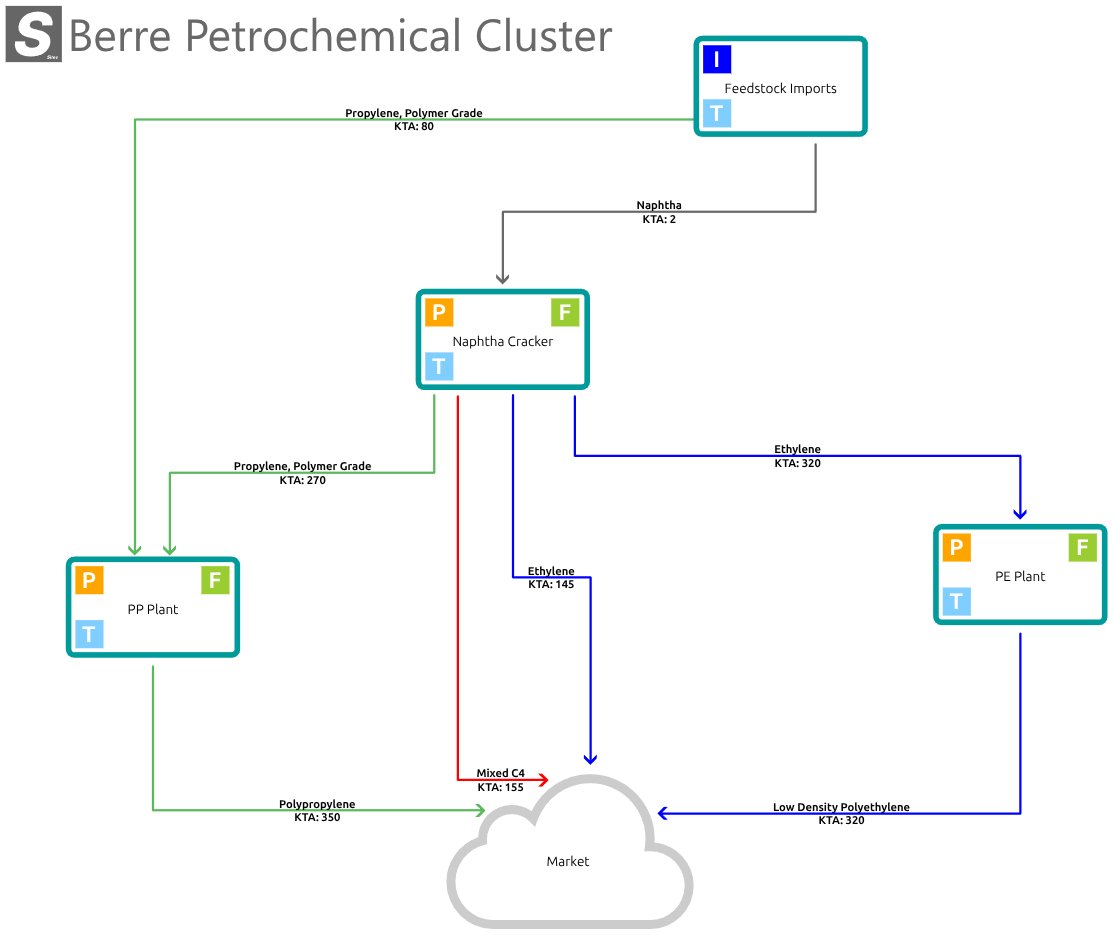

Berre Petrochemical Cluster Process Flow Diagram | ppPLUS Interactive Visualization Tool

Outlook: More Closures Ahead

The European petrochemical sector is entering a “new normal” characterized by ongoing rationalization. With many crackers and polymer plants facing existential threats due to age, size, and economics, further closures are likely. LYB’s asset sale could be a bellwether for additional portfolio actions across the industry.

How ppPLUS Can Help

For investors and stakeholders evaluating LyondellBasell’s divested assets, Portfolio Planning PLUS (ppPLUS) offers tailored economic modelling capabilities to assess risks, opportunities, and transaction value. ppPLUS specializes in developing site-specific models that integrate:

Asset configurations: Detailed analysis of production units, technologies (e.g., Steam Crackers at Berre and Münchmünster, Novolen Gas-Phase PP at Tarragona, Hostalen ACP HDPE at Münchsmünster, Lupotech T LDPE and Spheripol Bulk-Slurry PP at Berre), and feedstock flexibility.

Capacity utilization: Scenario-based projections accounting for market demand, regulatory constraints, and operational synergies.

Financial and operational metrics: Capex/opex forecasting, decarbonization cost avoidance, and liability assumptions (e.g., pensions, environmental obligations).

Using ppPLUS’s interactive platform, users can:

- Generate gross margin models for individual sites or combined portfolios.

- Simulate the impact of energy price volatility, carbon pricing, and feedstock availability.

- Benchmark asset performance against industry standards and regional competitors.

ppPLUS’s tools align with global best practices in economic modelling, including compliance with frameworks like the UK’s TAG M5.3 supplementary economic modelling guidelines for rigorous validation and scenario testing.

Explore ppPLUS’s asset-specific insights:

Contact ppPLUS to leverage its expertise in petrochemical asset valuation, strategic due diligence, and regulatory risk assessment for informed decision-making in this transformative transaction.

#portfolioplanningplus #ppplus #transactions #divestment #marginanalysis #economicmodelling #capacityutilization #opex #capex #lyondellbasell #sabic #indorama #ineos #exxonmobil #aequita #aramco