Ghana's Refining Outlook: Three Concurrent Projects Facing Execution Challenges

- Site

- Sentuo Refinery

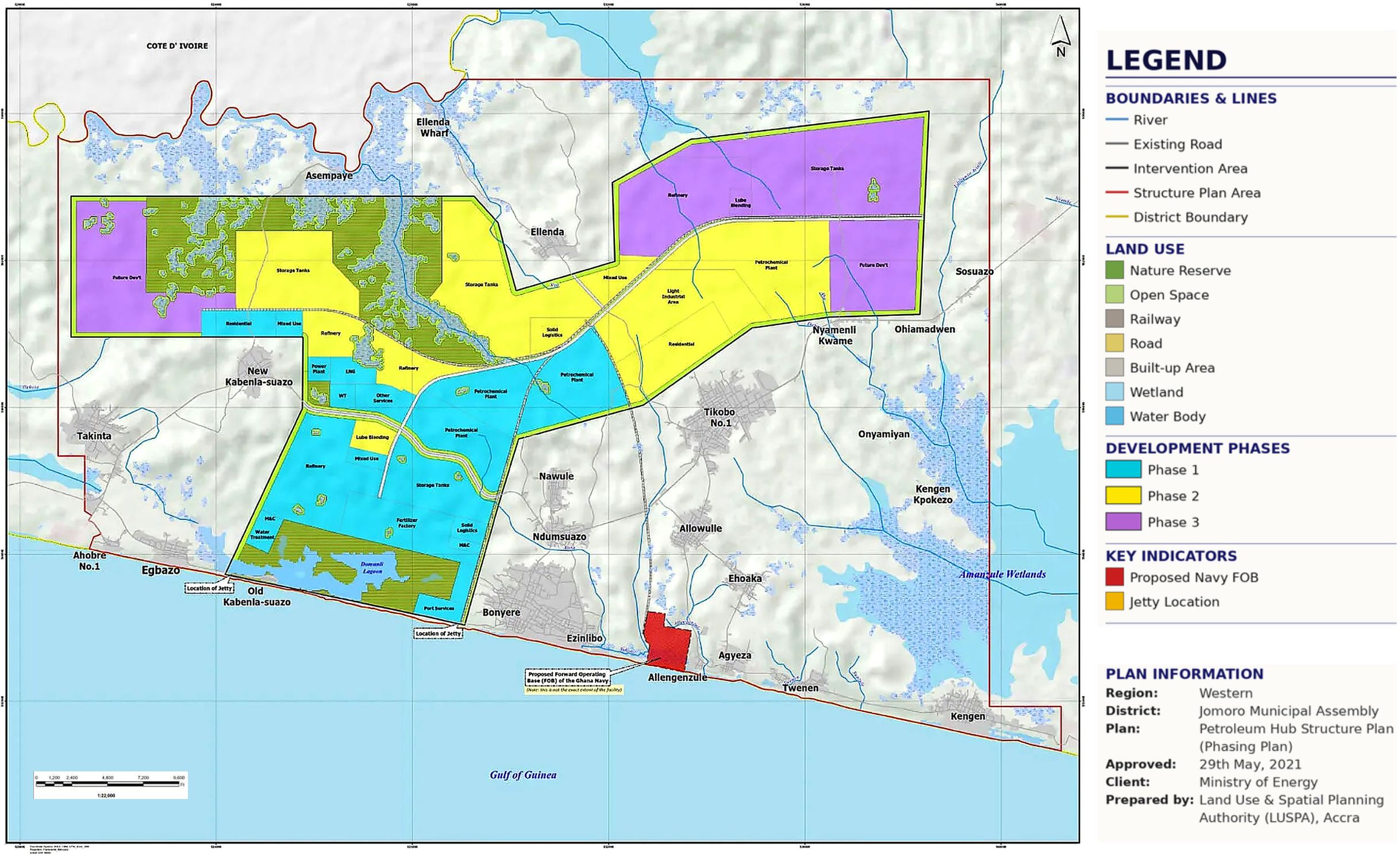

PHDC Petroleum Hub Structure Plan (Phasing Plan) | Adapted from: Land Use and Spatial Planning Authority (May 2021)

Ghana's Refining Industry Overview

Two refineries are currently operating in Tema, Ghana's industrial port city east of Accra.

TOR — the 63-year-old, state-owned Tema Oil Refinery came back to life in December 2025 after years of inactivity, currently processing 28,000 bpsd out of its 45,000 bpsd nameplate capacity. Full restoration to 45,000 bpsd awaits the tie-in of a newly installed furnace. A medium-term upgrade to 60,000 bpsd requires a new air-cooler unit still to be procured and installed. TOR's return was a genuine milestone — referenced in President Mahama's 2026 State of the Nation Address — but it is still a facility running well below its potential.

Tema Oil Refinery | Credit: CITI NEWSROOM

SORL — Sentuo Oil Refinery, a Chinese privately-owned plant commissioned in January 2024 — is the real workhorse. Operating at 40,000 bpsd under Phase 1 and accounting for 65% of all locally refined petroleum products in Ghana in 2024, it is currently commissioning its Phase 2 train which will bring total capacity to 80,000 bpsd. Phase 3, adding another 40,000 bpsd to reach a 120,000 bpsd total, was announced in July 2024 with a $980 million investment commitment.

Combined, even at full current capacity, Ghana's two Tema refineries supply a fraction of West Africa's daily consumption — roughly 90% of which is still imported.

Three New Projects, One Market

On top of what already exists, three major capacity additions are in various stages of planning and construction:

SORL Phase 3 — already committed and privately financed by Sentuo Group, this adds a third 40,000 bpsd train to bring SORL to its full 120,000 bpsd nameplate capacity.

Sentua Oil Refinery | Sentuo web site, learn more page (accessed May 27, 2026)

TOR's new 100,000 bpsd refinery — announced in January 2026, this would be a brand-new processing unit built alongside the existing TOR plant at Tema, raising TOR's total capacity from 60,000 to 160,000 bpsd. It would include a dedicated petrochemical plant. No financing structure, EPC contractor, or process licensor has been publicly announced. There is no confirmed timeline.

Ghana Petroleum Hub — Jomoro Phase One — the flagship: a $12 billion, 300,000 bpsd integrated cracking refinery and petrochemical complex in Jomoro, Western Region. Developed by the TCP-UIC Consortium (Touchstone Capital + UIC Energy Ghana + Chinese EPC contractors) under a concession from the state body Petroleum Hub Development Corporation (PHDC). Phase One alone covers a 5,000-hectare free zone site and includes tank farms (3 million m³), a marine terminal, petrochemical plants (90,000 bpsd), LNG, power generation, and lube blending.

The Jomoro Reality Check

The Jomoro Petroleum Hub is the boldest downstream project on the African continent — and by some distance the most complex to execute. Conceived as a full industrial free zone rather than a standalone refinery. The full three-phase hub ultimately envisages three integrated refinery and petrochemical clusters with a combined refining capacity approaching 900,000 bpsd, targeting completion by 2036. At that scale, Jomoro would rank among the top ten refinery complexes globally and transform Ghana into a net exporter of refined products and petrochemicals to the entire West African sub-region.

PHDC Petroleum Hub Structure Plant (Phasing Plan) | Adapted from: Land Use and Spatial Planning Authority (May 2021)

The path to that outcome, however, runs through a series of near-term hurdles that have proved more persistent than the August 2024 groundbreaking ceremony suggested. As of April 2026, the Executive Instrument legally transferring the project land to the state had only just been published — a prerequisite for any physical construction to begin. Community compensation payments to affected landowners in Jomoro remain outstanding, and the land size itself was revised downward from 20,000 to 12,356 acres (5,000 ha) following community negotiations and a presidential directive.

Absent an official commissioning date target for Phase One, PHDC CEO Dr. Toni Aubynn has declared 2026 the "Year of Action" in January 2026— physical site works are targeted to begin before year-end, with the land transfer process expected to conclude by July 2026. While some industry analysts cite 2028 as a commissioning target, ppPLUS considers 2030–2031 a more realistic timeline for Phase One first production, reflecting the time required to complete land acquisition, mobilise EPC contractors, close project financing, and commission a refinery complex of this scale and technical depth. The window is short, and execution discipline from this point forward will be the determining factor.

TOR vs. Jomoro: Competing State Priorities

Here is where it gets uncomfortable. TOR's proposed 100,000 bpsd new unit and the Jomoro Phase One refinery are — in fundamental terms — competing for the same things: West African export market share, domestic crude supply from Ghana's Jubilee and TEN offshore fields, skilled petroleum engineering labour, and government political bandwidth.

Jubilee and TEN offshore fields | Source: Tullow, via MarineLink (May 21, 2018)

Ghana's domestic fuel consumption sits at approximately 65,000–80,000 bpsd. Every barrel refined beyond that needs to be exported. The target export market — West Africa — is the same one that Nigeria's Dangote Refinery (operational since 2024, full nameplate capacity of 650,000 barrels per day reached in February 2026) is already aggressively targeting from a far larger domestic base.

If all announced projects proceed, by 2030 Ghana's theoretical refining capacity would reach:

| Facility | Capacity |

|---|---|

| TOR (upgraded existing) | 60,000 bpsd |

| TOR new refinery | 100,000 bpsd |

| SORL (all three phases) | 120,000 bpsd |

| Jomoro Phase One | 300,000 bpsd |

| Total | 580,000 bpsd |

Against domestic demand of 65,000–80,000 bpsd, that is a 7× to 9× oversupply relative to local consumption — entirely dependent on export markets absorbing the difference.

The strategic case for Jomoro is clear: it is designed from the ground up as an export-oriented free zone complex, with a marine terminal and the scale to compete regionally. The case for TOR's new unit is less obvious. It risks duplicating what Jomoro already plans to deliver — but with state capital, at a smaller scale, from a site that is 350 km from the hub and not inside a free zone.

Ghana Refining's Bottom Line

Ghana does not lack ambition in refining. What it lacks is a coherent national sequencing strategy — one that says plainly which projects get prioritised, which crude goes where, and how the state manages the inherent tension between backing PHDC's Jomoro vision and simultaneously asking TOR to expand into the same market.

The components of a genuine refining transformation exist. The architecture that connects them does not yet.

ppPLUS monitors the downstream sector across West Africa. This review is based on publicly available sources including PHDC, TOR, SORL corporate communications, AllAfrica, Ghana Upstream Petroleum Chamber, and The High Street Journal.