The Petroline Under Fire: How the Middle East Conflict Is Dismantling the Global Energy Architecture

- Site

- Yanbu Refinery

An oil tanker burns after being hit by an Iranian strike in the ship-to-ship transfer zone at Khor al-Zubair port near Basra, Iraq, late Wednesday, March 11, 2026. (AP Photo)

The Conflict in Context

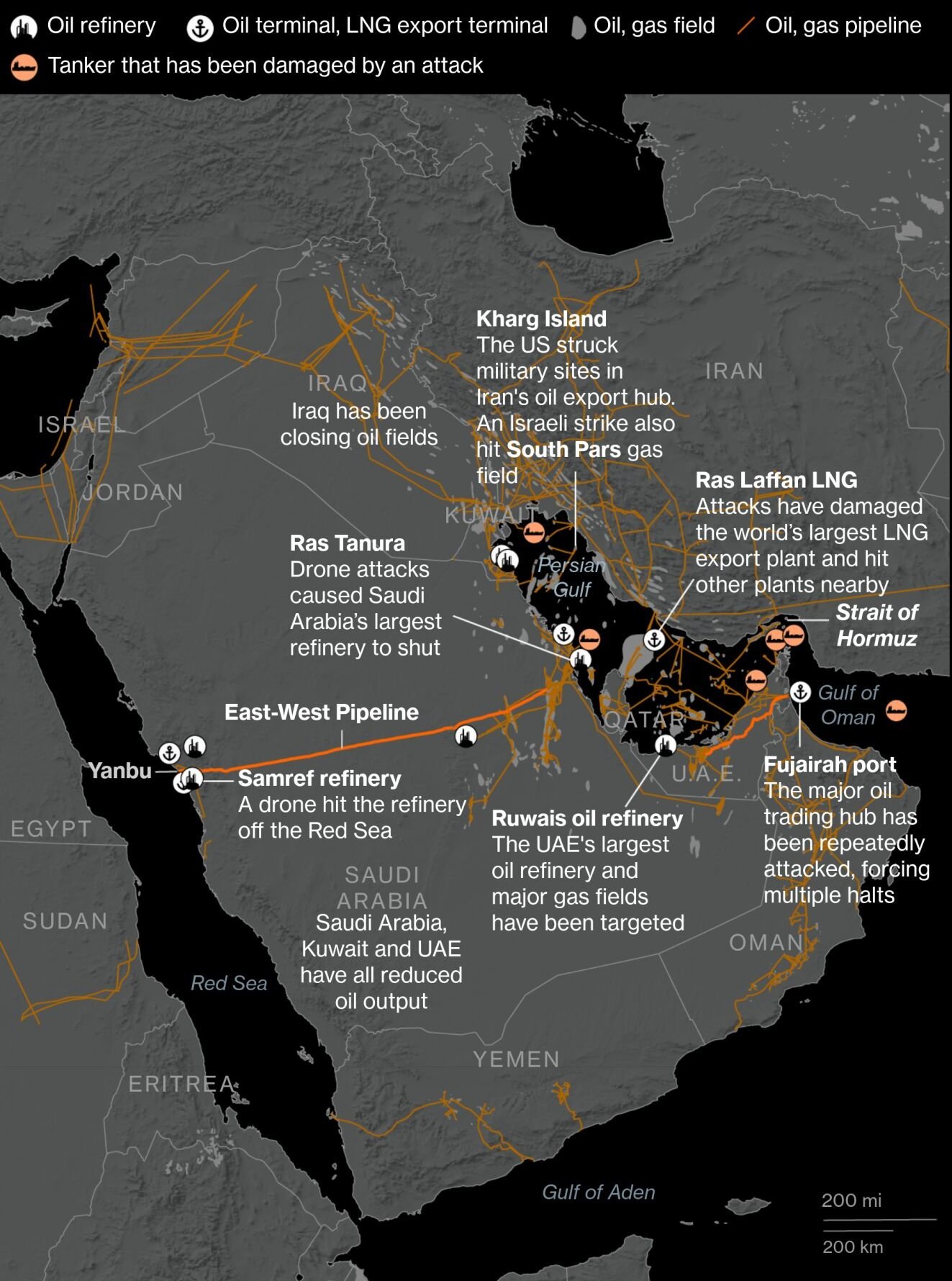

On 28 February 2026, the Strait of Hormuz — through which approximately 20% of the world's oil flows — was effectively blockaded by Iran following U.S.-Israeli airstrikes that killed Supreme Leader Ali Khamenei. In retaliation, Iran launched a sustained campaign of missile and drone strikes against energy infrastructure across the Gulf, targeting the oil and gas assets of Saudi Arabia, Qatar, Bahrain, Kuwait, and the UAE. What began as a geopolitical confrontation has since evolved into the world's most severe energy infrastructure crisis in decades.

Confirmed Facility Damage Across the Region

Saudi Arabia: The Epicentre

On 9 April 2026, Saudi Arabia's Ministry of Energy has — for the first time — put official numbers on the damage. The confirmed losses are staggering in scope, spanning upstream production, midstream pipelines, refining, petrochemicals, and power infrastructure across the Eastern Province, Riyadh, and Yanbu Industrial City.

Upstream Production (~600,000 b/d lost):

- Manifa offshore field — approximately 300,000 b/d in production capacity destroyed

- Khurais field — approximately 300,000 b/d in production capacity destroyed, bringing the total upstream loss to 600,000 b/d

Midstream — The Petroline (East–West Pipeline):

- A pumping station along the 1,200 km Petroline was struck by a drone on 9 April 2026, cutting approximately 700,000 b/d in throughput

- The pipeline had been operating at near-emergency capacity — up to 7 million b/d — to compensate entirely for the Hormuz closure, and was carrying ~4.6 million b/d in export loadings from Yanbu in late March

- The attack, critically, occurred just hours after a US-Iran ceasefire was reportedly agreed — signalling that infrastructure targeting is continuing independently of diplomatic frameworks

| Figure 1: Energy disruptions in the Middle East | Sources: Bloomberg reporting, Institute for the Study of War and AEI’s Critical Threats Project; US Central Intelligence Agency; US Department of Energy. via Insurance Journal (April 7, 2026) |

Refining (~550,000+ b/d capacity offline):

- Ras Tanura refinery (Saudi Aramco) — offline, approximately 550,000 b/d refining capacity

- SATORP refinery (Jubail) — targeted, exports of refined products disrupted

- SAMREF refinery (Yanbu) — attacked directly at the western export hub

- Riyadh refinery — attacked, further constraining domestic supply chains

NGL / Petrochemicals:

-

Ju'aymah processing facilities — struck by fires, directly impacting exports of LPG and NGL. Ju'aymah is one of Saudi Arabia's principal NGL fractionation and export terminals, making this loss particularly consequential for petrochemical feedstock supply chains globally.

Aramco CEO has characterised a sustained Hormuz closure as having "catastrophic consequences" for global oil markets.

Qatar: LNG Architecture Shattered

Qatar — supplier of roughly 22% of the world's LNG — has suffered some of the most structurally severe damage in the conflict.

Figure 2: Satellite imagery capture of Ras Laffan LNG production trains destruction on 18 March 2026 | Source: Mizar Vision

- On 2 March 2026, drone strikes hit the Qatar Energy's Ras Laffan Industrial City, forcing a complete halt of all 77 MTPA of Ras Laffan LNG production and a broad force majeure declaration

- By 18 March, Iranian missile attacks permanently damaged two LNG production trains — representing 17% of Qatar's LNG capacity, or 12.8 MTPA — with repair timelines estimated at 3–5 years

- A gas-to-liquids (GTL) unit at Pearl GTL jointly owned by QatarEnergy and Shell was also knocked offline, removing approximately 140,000 b/d of liquid products (naphtha, kerosene, propane, butane, fuel oil) — with a repair timeline of up to one year

- QatarEnergy has declared force majeure on long-term LNG contracts with South Korea, Belgium, China, and Italy. Analysts estimate up to 30% of Qatari LNG production could be lost across 2026, representing roughly 11% of global LNG supply

Bahrain: BAPCO — The Kingdom's Only Refinery, Hit Three Times

Bahrain's BAPCO Energies — operator of the country's sole refinery at Sitra Island, recently upgraded to 405,000 b/d from 267,000 b/d — has been struck in three separate attacks since the conflict began. The first Iranian missile strike hit the facility on 5 March, setting parts of the refinery ablaze. A second drone attack followed on 9 March, prompting BAPCO to formally declare force majeure on all group operations — citing the "ongoing regional conflict and the recent attack on its Refinery complex" — while confirming domestic fuel supplies remain secured. A third strike on 5 April ignited a major oil storage tank, with explosions also reported at the adjacent ALBA aluminium smelter and areas near the US Fifth Fleet headquarters at Manama. The April attack triggered a renewed force majeure declaration on exports.

Figure 3: Bahrain’s state-run Bapco Energies declared force majeure after attacks last month at the Sitra refinery | Source: Reuters

UAE and Kuwait: Storage Constraints Force Output Cuts

Neither the UAE nor Kuwait has been spared. Both countries — lacking the Petroline bypass option available to Saudi Arabia — have been forced into involuntary production curtailments driven by storage saturation and logistical paralysis.

-

ADNOC began "managing offshore production levels" in early March, a euphemism for cuts, citing storage constraints. The Abu Dhabi-Fujairah pipeline (1.5 million b/d bypass capacity) is operating at maximum, but is insufficient to cover the full export volume normally transiting Hormuz

-

Kuwait Petroleum Corporation declared force majeure on oil and refined product sales contracts. Kuwait's entire export infrastructure is Hormuz-dependent — there is no bypass pipeline. On 5 April, the Shuwaikh oil complex was directly attacked, disrupting Kuwait's limited remaining export capabilities

-

The Mina Al-Ahmadi refinery (340,000 b/d) and Mina Abdullah refinery (270,000 b/d) — Kuwait's two principal refining facilities, both located on the Gulf coast — have been struck by Iranian drone and missile attacks on 5 April alongside the Bahrain BAPCO strikes, compounding the country's already critical logistical paralysis with direct physical damage to its downstream infrastructure

-

Kuwait's long-planned 3–3.5 million b/d expansion programme is now considered at material risk of collapse

The Shift in Trading Routes

The conflict has triggered the most rapid and dramatic restructuring of oil trade flows since the 1970s.

| Route | Pre-Crisis Status | Current Status |

|---|---|---|

| Strait of Hormuz | ~20 million b/d transiting | Effectively blockaded since 28 Feb 2026 |

| Saudi Petroline → Yanbu | ~2.5 million b/d (normal export) | Surged to ~4.6–7 million b/d before attack |

| UAE Habshan–Fujairah Pipeline | Under-utilised (1.5 mb/d capacity) | Operating at maximum capacity |

| Red Sea (Yanbu loadings) | Regional export hub | Now primary Saudi crude export artery, but under attack |

| LNG tanker routes from Ras Laffan | 77 MTPA normal exports | Severely disrupted; force majeure in force |

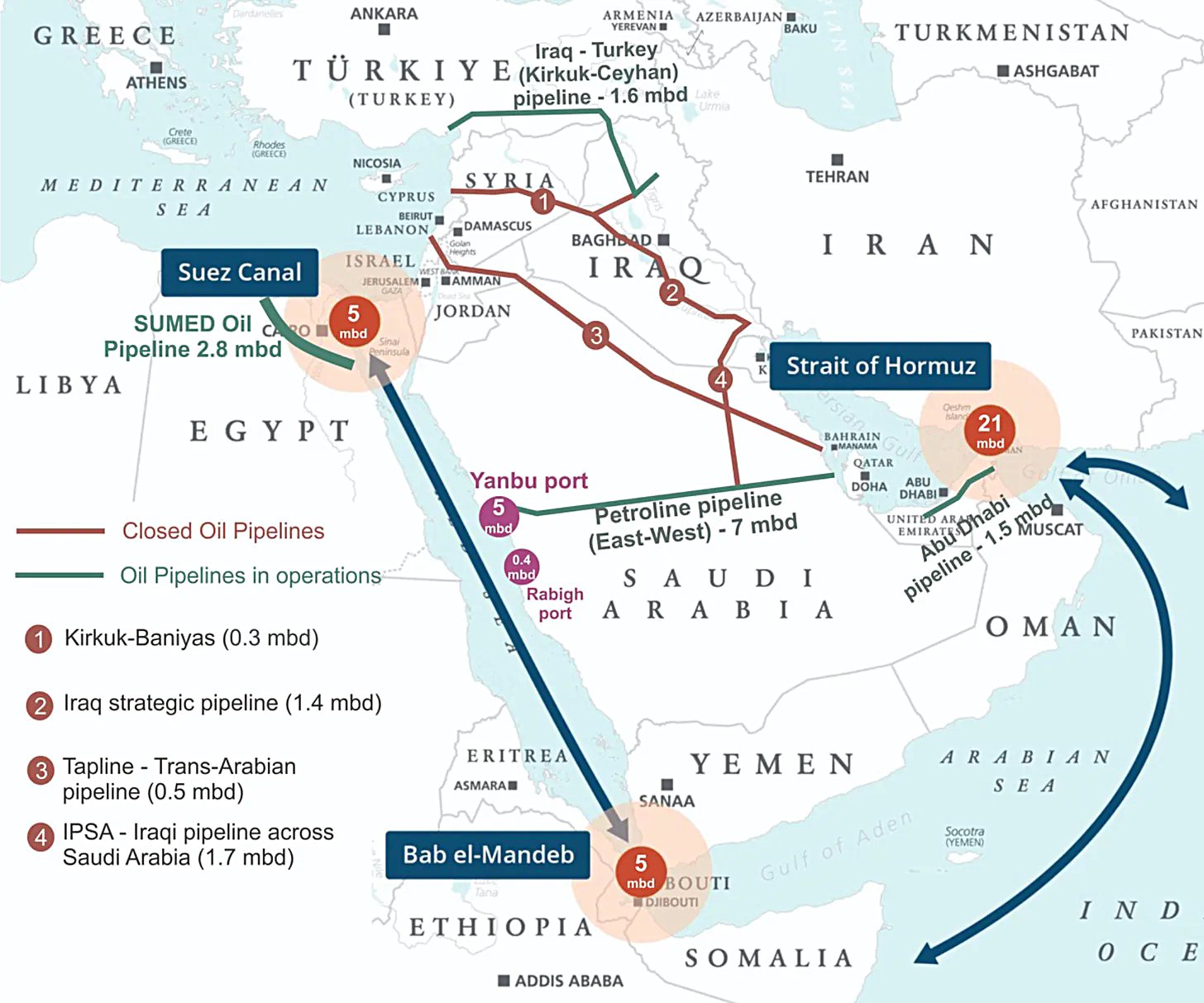

Figure 4: Middle East’s Tier 1 pipelines and maritime chokepoints (Bab el-Mandeb, Hormuz, and Suez)

Source: Mihail Stoyanov (April 3, 2026), The OldEconomy Substack

European and Asian buyers have been scrambling to source replacement LNG cargoes — with estimates suggesting 11% of global LNG supply has been removed from markets for up to five years. The ramifications for European energy security, which had only recently diversified away from Russian pipeline gas toward Qatari LNG, are profound.

Supply Disruption: The Running Total

Aggregating confirmed and reported losses across the region, the cumulative disruption to global supply is now material:

- ~600,000 b/d Saudi upstream production capacity lost (Manifa, Khurais)

- ~700,000 b/d Saudi Petroline throughput lost (East–West pipeline attack)

- ~550,000 b/d Saudi refining capacity offline (Ras Tanura alone)

- ~140,000 b/d Qatar GTL liquids removed for up to one year

- ~12.8 MTPA Qatar LNG capacity offline for 3–5 years

- UAE and Kuwait: unquantified but confirmed production curtailments

- Saudi NGL/LPG exports disrupted at Ju'aymah

Emergency and strategic inventories across consuming nations are being drawn down at an accelerating pace. Saudi Arabia's Ministry of Energy has explicitly warned that "a significant portion of operational and emergency inventories" has already been depleted, "affecting the availability of supplies and limiting the ability to respond to this supply shortfall".

Figure 5: The role of Hormuz for the global economy, share of imports and exports

Source: Mihail Stoyanov (March 6, 2026), The OldEconomy Substack

Forward Risk: What Happens If the Blockade Continues?

The most consequential forward-looking risk is not the damage already done — it is the systematic degradation of redundancy. The global oil architecture was designed with layers of backup. Those layers are being methodically stripped away.

1. The Petroline Is Now the Last Artery — and It Has Been Hit

The East–West pipeline was engineered precisely as the Hormuz bypass of last resort. With Hormuz closed, it had been running at near-full emergency capacity. It has now been struck. A second, more damaging attack on the Petroline — or on the Yanbu loading terminal itself — would leave Saudi Arabia with no viable large-scale crude export route. This is not a theoretical scenario; it has already been attempted once and partially executed.

2. Saudi Production Curtailments Are Beginning

Informal reports suggest Saudi Arabia is beginning to curtail production as storage at Eastern Province terminals — cut off from Hormuz — fills to capacity. The Petroline, even at 7 million b/d, cannot absorb Saudi Arabia's full 12+ million b/d production. The excess has nowhere to go.

3. Qatar's LNG Exports Are Structurally Impaired for Years

The damage to Ras Laffan's LNG trains is not a weeks-long disruption — it is a multi-year structural loss from the global LNG supply balance. European utilities, South Korean and Japanese power generators, and Chinese industrial consumers face years of supply shortfalls that cannot be fully compensated by U.S. LNG or Australian supply alone.

4. Kuwait Has No Bypass and Its Infrastructure Is Now Being Targeted

Kuwait's total dependence on Hormuz — combined with the April attack on the Shuwaikh complex — means that sustained conflict would effectively remove Kuwait from the export market entirely.

5. The Petrochemical and NGL Supply Chain Is Fracturing

LPG, NGLs, and GTL products — critical feedstocks for the global petrochemical industry — are being removed from the market simultaneously from multiple sources: Ju'aymah (Saudi Arabia), Ras Laffan GTL (Qatar), and Kuwaiti refineries. Petrochemical plants in Asia and Europe that rely on Gulf-sourced naphtha, propane, and butane face the prospect of feedstock rationing.

Historical Parallel: Echoes of 1973 and 1979

The 1973 Arab oil embargo and the 1979 supply shock triggered by the Iranian Revolution each demonstrated that politically-driven Gulf supply disruptions carry consequences far beyond their immediate geography. This crisis is structurally more dangerous on several dimensions: it involves simultaneous damage to production, midstream, refining, and LNG infrastructure across multiple sovereign producers; it targets the bypass infrastructure that was itself built as the lesson of 1973; and it is unfolding against a backdrop of already-depleted strategic reserves and a more financialised, just-in-time global energy system.

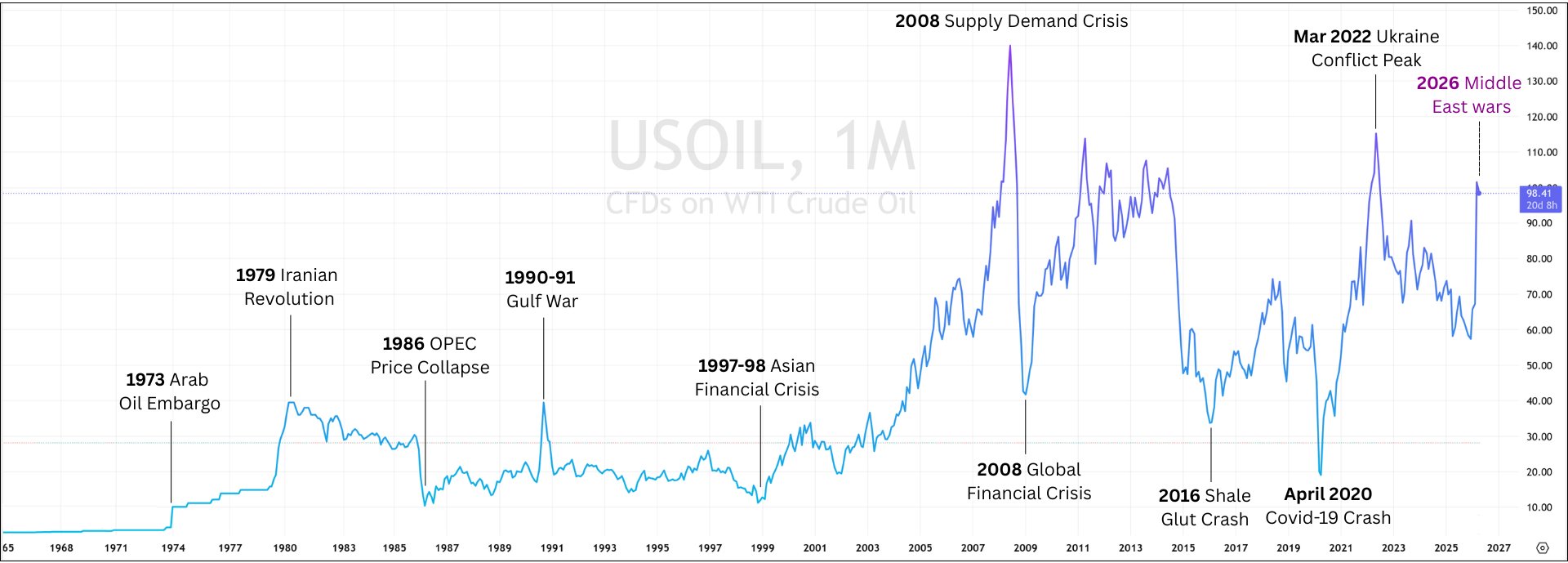

Figure 6: CFDs on WTI Crude Oil (monthly close prices as of April 10, 2026) | Source: TradingView, labels by ppPLUS

The world has not faced a disruption of this breadth, depth, and simultaneity since the crises of the 1970s. The difference is that those crises involved embargoes — deliberate decisions to withhold supply. This one involves the physical destruction of the infrastructure through which supply flows. That distinction matters enormously for the speed and completeness of recovery.

ppPLUS monitors energy infrastructure, technology, and corporate developments across the global oil, gas, and petrochemical sector. This article draws on official Saudi Ministry of Energy statements, Reuters, Bloomberg, CNBC, Times of India and industry sources.