Global LNG in Crisis: Cascading Disruptions from the March 2026 Middle East Conflict

The Conflict: How It Started

The crisis was triggered by a US-Israeli military campaign against Iran, launched on 28 February 2026. Iran responded with a sweeping retaliatory strike strategy targeting the energy infrastructure of US allies across the region — choosing economic pain over direct military counter-escalation. The resulting chain of energy infrastructure attacks has progressively widened, drawing in Qatar, Saudi Arabia, Iran itself, and extending as far as the Mediterranean Sea.

Qatar: The World's Largest LNG Hub Goes Dark

The most consequential single event was Iran's drone and missile strike on QatarEnergy's Ras Laffan LNG — the world's largest LNG complex — on 2 March 2026. All 14 LNG trains at Ras Laffan, representing 77 MTPA (~20% of global LNG supply), were immediately shut down. Simultaneously, QatarEnergy's downstream operations at Mesaieed Industrial City — including the Messaied crude oil refinery, SEEF chemical plant, and associated facilities — were halted.

LNG trains at Ras Laffan LNG | Source: QatarEnergy LNG

QatarEnergy declared force majeure on all LNG export contracts on 4 March — the first such declaration in its history. Restarting the world's largest LNG hub is no simple task: the cryogenic cooldown and sequential train restart process requires a minimum 4 weeks from the decision to resume operations. As of today, no restart announcement has been made.

The Strait of Hormuz — the only viable exit route for Qatari LNG — has seen zero commercial LNG transits since 28 February, with vessel traffic falling to a single recorded transit on 12 March. Major container lines including Maersk, CMA CGM, and Hapag-Lloyd have suspended all Hormuz transits and rerouted via the Cape of Good Hope, adding 10–14 days to voyage times and absorbing significant fleet capacity. The strategic chokepoint through which ~20% of global LNG and ~20% of global crude normally flows is effectively closed.

The disruption has also forced QatarEnergy to delay the first production from its landmark North Field East (NFE) expansion — four new 8 MTPA trains that would have raised Qatar's capacity to 126 MTPA — from mid-2026 to at least early 2027.

Persian Gulf's LNG Import & Export Terminals | Source: U.S. Energy Information Administration, via Cocklin M., Natural Gas Intelligence (Mar 6, 2026)

Saudi Arabia: Ras Tanura and LPG Exports Hit

On the same day as the Qatar strikes, Iranian drones hit Saudi Aramco's Ras Tanura refinery in the Eastern Province — the world's largest oil refinery by throughput — taking out two refinery units. Aramco's Juaymah LPG terminal, one of the world's largest natural gas liquid export hubs, was structurally damaged and halted LPG exports. The combined Gulf energy strikes sent Brent crude surging to $105.87/barrel — a level last seen in 2022 — within hours of the attacks.

Ras Tanura | Source: Aramco website

Russia: LNG Tanker Sunk in the Mediterranean

A significant and geographically unprecedented escalation occurred on 4 March 2026, when the Russian-flagged LNG carrier Arctic Metagaz — carrying approximately 60,000 tonnes of LNG from Murmansk, destined for European markets — was struck by Ukrainian sea drones and sunk approximately 240 km off the Libyan coast, between Libya and Malta. All 30 Russian crew members were rescued and transferred to vessels heading to Benghazi.

The attack marks the first confirmed sinking of a Russian LNG tanker and represents the first extension of Ukraine's maritime drone campaign beyond the Black Sea into the Central Mediterranean — a dramatic expansion of the geographic scope of risk for Russian energy exports. The Arctic Metagaz was operating under sanctions imposed by Western governments. Russia condemned the attack as a "terrorist act" targeting civilian energy infrastructure; the incident compounded supply anxiety in an already severely stressed European gas market, adding further upward pressure to TTF prices at a moment when Qatari LNG had simultaneously gone offline.

Wreck of the Russian gas tanker "Arctic Metagaz" | Source: agenzia NOVA (Mar 4, 2026)

Iran: Kharg Island, Tehran Refineries, and Now South Pars

As the conflict deepened into its second week, US and Israeli strikes progressively targeted Iran's own energy infrastructure — removing Iran as a supply source while simultaneously degrading its economic war-fighting capacity:

-

8 March: Israeli strikes hit four oil storage facilities in Tehran and Alborz province, including the Tehran refinery and major oil depots, causing large fires

-

9 March: Iran shut down two Israeli gas fields following missile threats, disrupting gas exports to Jordan and Egypt

-

14 March: US forces struck Kharg Island — Iran's primary crude export terminal handling ~90% of Iran's ~1.4 million b/d of crude exports. While the US declared objectives "obliterated", Iran disputed the damage assessment and threatened retaliation

-

18 March (today): Iranian state media confirmed that facilities at South Pars gas field and the adjacent Asaluyeh petrochemical zone in Bushehr province were struck by US-Israeli projectiles. South Pars — the world's largest natural gas field, sharing the same geological structure as Qatar's North Field — accounts for the vast majority of Iran's domestic gas production. This marks the first confirmed strike on Iran's upstream gas production in the conflict, and represents a major escalation threshold

The full extent of damage at South Pars remains unconfirmed as of publication time.

Multiple fires continue in the Iranian part of the world 's largest South Pars oil and gas field after Israeli/US airstrikes | Screenshot from media report (Mar 18, 2026, 15h47 CET)

Market Impact: Prices and Supply in Crisis

The cumulative effect of all events has fundamentally repriced global energy in under three weeks:

| Benchmark | Pre-Crisis (Feb 2026) | 18 March 2026 | Change |

|---|---|---|---|

| TTF (European gas) | ~$10.8/MMBtu | ~$16.7/MMBtu | +55% |

| JKM (Asian LNG spot) | ~$10.9/MMBtu | ~$15.1/MMBtu | +39% |

| LNG spot | ~$15–16/MMBtu | ~$24/MMBtu | +50–60% |

| Brent crude | ~$77/barrel | ~$105.87/barrel | +37% |

| Hormuz LNG transits | ~18–20 vessels/day | ~0 | –100% |

Morgan Stanley, S&P Global, and Kpler have all revised the 2026 LNG market outlook from surplus to deficit. There is no meaningful short-term replacement supply: US LNG plants run near nameplate capacity with most volumes under long-term contracts; Australian producers cannot flex above committed volumes; no new major projects come online before 2027 at the earliest.

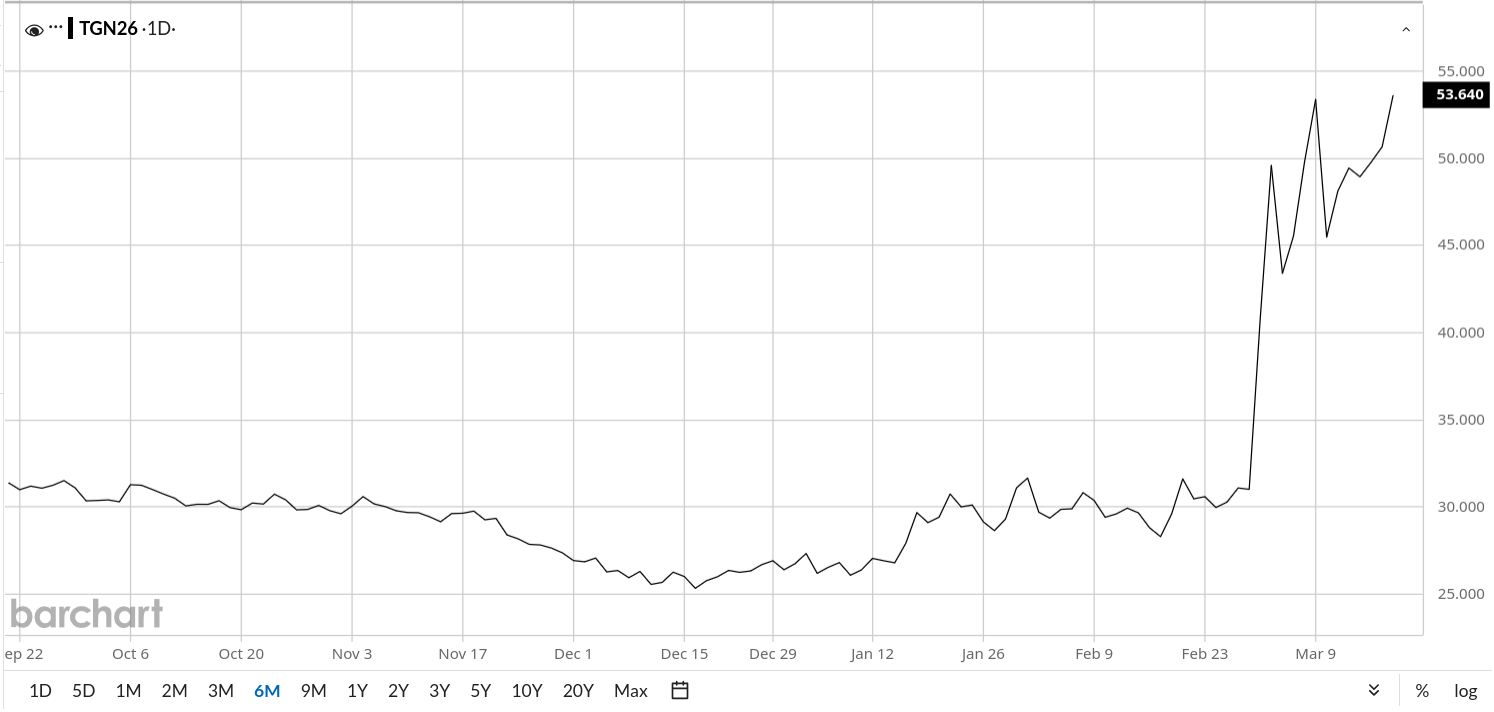

Dutch TTF Natural Gas Futures — July 2026 contract | Source: Barchart (11:41 CT [ENDEX], Chart for Wed, Mar 18th, 2026)

Structural Vulnerabilities Exposed

The crisis has laid bare three long-standing structural weaknesses in the global gas and LNG system that will drive industry strategy for years to come:

-

Chokepoint dependency: Over 40% of globally traded LNG passes through or originates within 500 km of the Strait of Hormuz — a single maritime chokepoint with no bypass alternative for Middle East producers

-

Single-hub concentration: Qatar's entire 77 MTPA capacity sits at one industrial city (RLIC), connected to global markets through the Hormuz Strait alone — a vulnerability now fully exposed

-

Thin spot market liquidity: Despite years of LNG market growth, global spot trading remains insufficiently liquid to absorb a shock of this magnitude; the 55% TTF spike reflects the absence of swing supply capacity

Outlook

The duration of the immediate disruption hinges on the geopolitical resolution of the US/Israel-Iran conflict and the reopening of the Strait of Hormuz — both entirely beyond QatarEnergy's or the market's control. Even under an optimistic ceasefire scenario this month, the physical restart of Ras Laffan would require a minimum of four further weeks, while the newly attacked South Pars facilities may take considerably longer to restore. Critically, the destruction of energy infrastructure has not stopped: each successive strike on Gulf and Iranian assets deepens the supply deficit, extends the recovery timeline, and raises the structural floor for energy prices.

Critically, the destruction of energy infrastructure has not stopped. The cumulative effect of these strikes — the removal of Qatar's 77 MTPA, the closure of the Strait of Hormuz, the degradation of Iranian gas infrastructure, and the targeting of Russian LNG shipping — has created a structural supply deficit with no credible short-term remedy. Each successive destruction of assets deepens the supply deficit, extends the recovery timeline, and raises the structural floor for energy prices, giving rise to a new LNG price regime.

The 2026 market entered the year with buyers confidently negotiating under a forecast surplus; that world no longer exists. Pricing power has shifted decisively and durably back to sellers, and a geopolitical risk premium is now permanently embedded in both spot and long-term contract valuations. The scramble to secure supply from non-Hormuz-dependent sources is already underway, and buyers who hesitated on long-term commitments during the surplus era now face a market where supply security commands a premium that may define LNG contract economics for the remainder of this decade.

This report draws on information from the following sources: Reuters, Bloomberg, Associated Press, Al Jazeera, The New York Times, The Times of Israel, DW News, WTOP, S&P Global Commodity Insights, Kpler, OilPrice.com, MEES, Argus Media, MEED, LNG Global, AInvest, Petroleum Australia, BizExtract, Maersk, Windward AI, Ship & Bunker, Morgan Stanley, Yahoo Finance, Fastmarkets, and the official QatarEnergy website (qatarenergy.qa). All sources are open-access and publicly available. Information on the South Pars attack (18 March 2026) is based on breaking reports and remains subject to verification.