The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

Helium is a crucial component for semiconductor manufacturing and there are no available substitutes, according to the Semiconductor Industry Association.

A.I. enhanced image with helium symbol | Stock photo: Farrington M., techUK (Jul 2, 2024),

Helium occupies a paradoxical position in the global economy: it is simultaneously one of the most strategically critical industrial gases and one of the least visible to policymakers and the public. As the semiconductor industry enters a new era driven by artificial intelligence, and as geopolitical fractures reshape supply chains from the Strait of Hormuz to the steppes of Siberia, helium has emerged as a hidden fault line in the global technology supply chain. This article examines helium's supply geography, its structural relationship with LNG infrastructure, the accelerating demand from the AI chip sector, the ongoing disruptions from Middle East conflict, and the broader shift from a US-dominated supply model to a fragmented multinodal market — a transition whose strategic implications are only beginning to be understood.

Helium's co-dependency with LNG is structural, not incidental. Helium is present in natural gas at concentrations typically ranging from 0.04% to 3%, and is recovered during the cryogenic liquefaction process used to produce LNG — meaning that any disruption to LNG processing, whether from conflict, technical failure, or trade restrictions, directly and immediately curtails helium output with no alternative recovery pathway. Helium supply is therefore a direct function of LNG economics, plant operational continuity, and trade flow stability. Major LNG-linked helium hubs include:

| Location | LNG Operator | Helium Plants | Annual He Capacity |

|---|---|---|---|

| Ras Laffan LNG, Qatar | QatarEnergy LNG | Helium 1, 2, 3 | ~74 Mm³ |

| Amur GPP, Russia | Gazprom (GPPB) | Amur He Units 1–3 | ~60 Mm³ (design) |

| Skikda/Arzew, Algeria | Sonatrach / Helison | He Plant | ~18 Mm³ |

| US Gulf/Midwest | ExxonMobil, Air Liquide, Air Products, Linde | Multiple | ~75–81 Mm³ |

When Qatar's Ras Laffan LNG terminal went offline in early March 2026 following the blockade of the Strait of Hormuz by Iran, helium prices surged and South Korean chip makers — who sourced 64.7% of their helium from Qatar in 2025 — were placed on a critical supply countdown estimated at two weeks of inventory. TSMC stated it did not anticipate immediate impact, while SK Hynix confirmed it had pre-diversified. The episode starkly illustrates the consequence of over-concentration in a single LNG hub.

LNG trains at Ras Laffan LNG | Source: QatarEnergy LNG

For most of the 20th century, the United States exercised near-total control over the global helium supply. The US Federal Helium Reserve (Bureau of Land Management), located beneath the Texas Panhandle, was the world's largest helium stockpile, accumulated from the 1920s onward under a national security mandate. At its peak, the US supplied over 70% of world production. The Helium Privatization Act of 1996 mandated the progressive sale and decommissioning of this reserve, a process completed in 2021. The consequences of this decision have been far-reaching: the US strategic buffer has been dismantled at precisely the moment when geopolitical competition over helium access is intensifying

Today, the United States produces approximately 75–81 million cubic metres per year, primarily from fields in Kansas (Hugoton), Wyoming, and Texas, with key operators including ExxonMobil, Air Products, Linde, and Air Liquide.

Qatar has emerged as the world's largest single-country helium exporter, producing approximately 45–50 million cubic metres per year as a byproduct of LNG processing at the Ras Laffan Industrial City complex. Three dedicated helium plants — Helium 1, 2, and 3 — operated by QatarEnergy LNG — extract helium from the gas streams of the North Field, the world's largest natural gas reservoir. QatarEnergy's ongoing North Field LNG expansion (targeting +48 MTPA additional LNG capacity by 2030) will more than double Qatar's helium capacity, and new long-term supply agreements — including a 300 million cubic feet/year deal with Air Liquide signed in January 2026 — confirm Qatar's ambition to dominate global helium exports for the next decade.

Ras Laffan liquid helium cryogenic tank containers | Source: QatarEnergy LNG

Gazprom's Amur Gas Processing Plant in Siberia, launched in stages from 2021, is designed to be the world's single largest helium production facility, with an ultimate capacity of 60 million cubic metres per year — representing roughly one-third of current global supply. Two of three helium production trains were commissioned in 2023, notably without Western licensors, following sanctions imposed after the start of the conflict in Ukraine. Gazprom reported production of approximately 6.3 million cubic metres in 2023, growing rapidly as trains ramp up.

Russia's Amur plant represents a classic dual challenge: it is the primary driver of the current market surplus, yet transactions with Russian entities are subject to Western sanctions, payment complications, and political risk. South Korean and Taiwanese chip manufacturers, who together account for 36% of global semiconductor capacity, face a difficult triage: Qatar supply is threatened by Hormuz blockade, US supply is insufficient to fill the gap at short notice, and Russian supply is politically and legally fraught.

Amur Gas Processing Plant trains 1, 2 and 3 as of July 2024 | Source: Gazprom, Youtube video

Tanzania's Rukwa Basin has emerged as potentially the most significant new primary helium deposit ever discovered, with unrisked prospective recoverable resources estimated at approximately 138 billion cubic feet (~3.9 billion cubic metres) — a transformative volume relative to current annual global consumption of ~6 billion cubic feet. Tanzania issued its first-ever helium mining licence to Helium One Global (London Stock Exchange listed) in early 2025 for the Rukwa Helium Project covering 480 km². Full-scale production was targeted for 2025, though infrastructure and logistics challenges remain significant in this landlocked, remote region.Unlike Qatari or Russian helium — which are byproducts of LNG or gas processing — Tanzanian helium is a primary deposit, formed by ancient radioactive decay in the East African Rift System's volcanic geology. This geological independence from LNG infrastructure is strategically important: Tanzania's helium production is not linked to, or disrupted by, events in LNG markets or the Strait of Hormuz

Additional emerging producers include:

China's approach to helium supply security is best understood not as reactive procurement, but as deliberate industrial policy — a structured multi-year effort to eliminate a critical dependency before it could be weaponized against Beijing's technology ambitions.

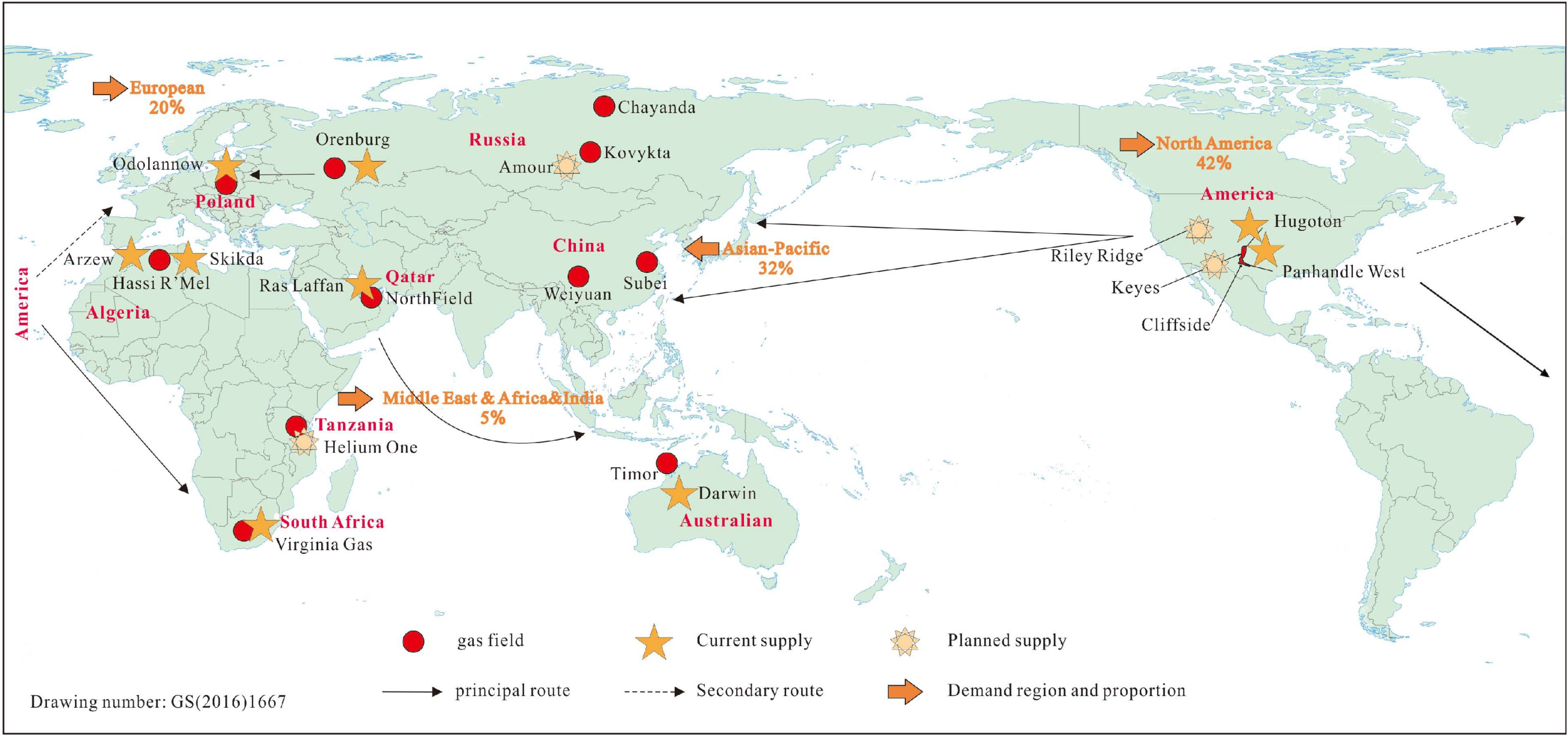

Schematic diagram of global major helium reservoir distribution and supply pattern

Source: Zhang, Y. et al. (Oct 23, 2024), Global Helium Industry Chain Analysis and Implications for China. Preprints. DOI: 10.20944/preprints202410.1799.v1

China's helium imports reached 4,924 tonnes in 2025 — a 21.7% year-on-year increase — reflecting the rapid expansion of its semiconductor and advanced manufacturing base. But import growth alone deepens dependency rather than resolving it. What distinguishes China's approach is the simultaneous construction of four parallel supply pillars:

Taken together, these four pillars represent a coherent sovereign supply strategy: diversified by geography, insulated from Western interdiction, and anchored by the world's largest emerging primary deposit and the world's largest new processing facility. China has systematically converted a critical vulnerability into a position of structural supply security — one that no single geopolitical event or Western policy instrument can now unravel.

Helium demand is increasingly concentrated in high-technology sectors where substitution is technically impossible, while legacy applications such as balloon inflation and welding are gradually declining in relative importance — a structural shift that makes the market simultaneously more resilient in volume terms and more strategically sensitive in criticality terms.

| Application | % of Global Demand | Trend |

|---|---|---|

| MRI & medical | ~23% | Stable/growing (recycling increasing) |

| Semiconductors & electronics | ~22% | Rapidly growing (AI chips) |

| Cryogenics & research | ~18% | Growing (quantum computing) |

| Aerospace & rocketry | ~10% | Growing |

| Fiber optics manufacturing | ~9% | Stable |

| Leak detection | ~6% | Stable |

| Welding (inert gas) | ~5% | Stable |

| Lifting gas (balloons) | ~4% | Declining |

| Other | ~3% | Mixed |

Global demand is projected to grow from approximately 6 billion cubic feet (~170 million m³) in 2025 at a compound rate of approximately 2.5% per year (Intelligas, 2025), reaching 8.0–8.5 billion cubic feet (~240 million m³) by 2030, driven primarily by semiconductor and quantum technology applications while partially offset by efficiency improvements in MRI and legacy sectors.

MRI and medical applications remain helium's largest end-use — but AI-driven quantum computing is emerging as a powerful new challenger.

Source: Vasco N. (Feb 17, 2025). westair

Helium's role in chip manufacturing is multiple and irreplaceable. It is used to:

No substitute exists for these functions due to helium's unique combination of inertness, thermal conductivity, and atomic size.

The AI semiconductor boom has qualitatively changed the demand profile for helium. Advanced chips — NVIDIA H100/H200 GPUs, AMD MI300X, and next-generation AI accelerators — are produced on 3–5nm nodes requiring far more process steps, longer fab times, and higher helium consumption per wafer than conventional chips. High-Bandwidth Memory (HBM), now commanding up to 70% of advanced memory production capacity in 2026, is similarly helium-intensive.

It is important to note, however, that overall market demand growth is more moderate than the semiconductor narrative alone might suggest: Intelligas Consulting projects aggregate helium demand growth at approximately 2.5% per year, as rapid growth in the chip and quantum sectors is partially offset by declining demand in legacy applications (balloon inflation, welding), improving recycling rates in MRI facilities, and efficiency gains in research institutions. The semiconductor sector is thus the critical marginal demand driver — not the whole picture.

Semiconductor wafer fabrication cleanroom, with robotic inspection-processing heads operating over silicon wafers | Credit: Jirasukhanont K., PhonlamaiPhoto's Images

Taiwan and South Korea together represent 36% of global semiconductor production capacity, yet both are almost entirely import-dependent for helium, and both have historically over-concentrated that supply in Qatar.

| Producer | Country | Products | Helium Exposure |

|---|---|---|---|

| TSMC | Taiwan | Logic (Apple, NVIDIA, AMD chips) | High — 18% of global capacity |

| Samsung | South Korea | Logic + HBM/DRAM/NAND | Very High — 64.7% He from Qatar |

| SK Hynix | South Korea | HBM (dominant) + DRAM | Very High — diversifying post-Hormuz |

| Micron | USA | DRAM, NAND | Moderate — domestic US supply available |

| Intel | USA | Logic (fabs in US, Ireland, Israel, Germany) | Moderate |

| Samsung/SMIC | China | Mature nodes (28nm+) | Growing |

Both Russia and China are investing heavily in domestic semiconductor capacity, precisely to reduce their dependence on Western-controlled chip supply chains — and therefore their indirect dependence on Western-controlled helium access:

The strategic implication is clear: both Russia and China are building closed-loop technological ecosystems in which helium — along with rare earths, advanced lithography equipment, and EDA software — is managed as a sovereign resource.

Amur Gas Processing Plant helium production as of July 2024 | Source: Gazprom, Youtube video

One of the most counterintuitive features of the current helium market is that statistical oversupply and acute supply security risk coexist simultaneously — a paradox that conventional supply/demand analysis fails to capture.

After three years of structural shortage (2021–2023), driven by the delayed ramp-up of Gazprom's Amur plant and the disruption caused by Western sanctions, the global helium market tipped into a modest surplus in 2024, with supply estimated at approximately 6.5 Bcf against demand of 6.0 Bcf (Intelligas Consulting, 2024). This surplus intensified in 2025, with Russian Amur volumes flooding Asian spot markets and some US producers curtailing output to avoid take-or-pay obligations at below-market prices.

Yet the same period saw spot market premiums for Grade 5.0–6.0 helium surge by 300–400% in Europe and East Asia, driven by geopolitical supply anxiety. Both phenomena are simultaneously true because the market has bifurcated structurally into two parallel pricing regimes:

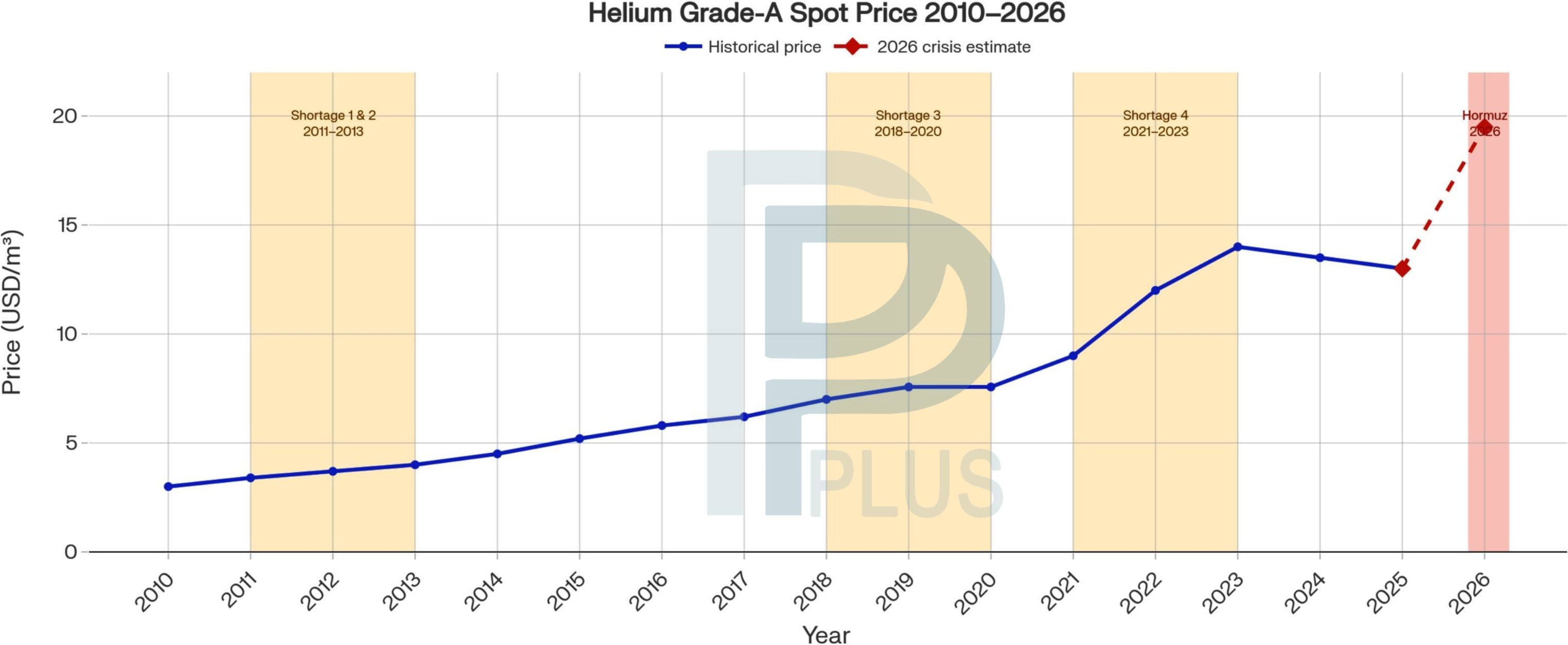

A.I. generated helium price chart based on the following price information sources: USGS · BLM · ChemAnalyst · Kornbluth Helium Consulting · Reuters Mars 2026

Legend: Shortage 1&2 (2011–2013): US BLM reserve drawdowns and infrastructure bottlenecks; Shortage 3 (2018–2020): Qatar embargo + US Federal Reserve depletion + delayed Qatar Helium 3 plant; Shortage 4 (2021–2023): Post-COVID logistics collapse + Russian supply constraints → record high ~$14/m³; Shortage 5 (2026 ongoing) Hormuz shock: Iranian attacks force QatarEnergy to halt Ras Laffan (~35% of world supply); spot prices surge to est. ~$19.50/m³ as of March 2026

⚠️ Note: Helium is predominantly traded on long-term contracts with limited spot market transparency. Prices shown reflect US BLM posted prices (2010–2019) and market indicative prices (2020–2026). The 2026 figure is an early-crisis estimate based on reported ~50% increase over the 2025 baseline; actual contract renegotiation prices may differ significantly. Historical prices in USD/m³ at standard conditions (0°C, 1 atm).

This bifurcation is explained by four converging factors:

The practical consequence: a market in nominal oversupply can simultaneously generate record spot prices, critical supply alerts, and geopolitical weaponization. Traditional supply/demand models are insufficient analytical tools for a resource that is simultaneously a commodity, a strategic material, and a geopolitical instrument.

The ongoing Iran conflict and the blockade of the Strait of Hormuz represent a Category 1 supply shock that transforms latent paradox into active crisis — exposing precisely the structural fragilities that the oversupply narrative had obscured. Key exposure vectors:

Persian Gulf's LNG Import & Export Terminals | Source: U.S. Energy Information Administration, via Cocklin M., Natural Gas Intelligence (Mar 6, 2026)

The helium market's response to the conflict in Ukraine in 2021–2022 — when Gazprom's Amur ramp-up was disrupted and prices spiked — demonstrated that the market has no meaningful strategic reserve and very limited demand-side flexibility, given helium's irreplaceability in fab processes. The March 2026 Hormuz blockade is a second, more acute demonstration of the same structural fragility: the oversupply that statisticians record and the shortage that procurement managers experience are, in helium, one and the same market.

Several converging forces define the helium market's trajectory:

The global helium market is transitioning from a US-centric, strategically managed resource to a multinodal, commercially competitive, and geopolitically contested one — in which the United States, Qatar, Russia, China, and emerging African producers each hold partial and conditional leverage. The oversupply paradox — where abundance and scarcity coexist — will be its defining characteristic for the remainder of this decade. For industries dependent on advanced chips — from AI data centres to autonomous vehicles to defence systems — helium supply security has quietly become a strategic priority.

The global helium market is transitioning from a US-centric, strategically managed resource to a multinodal, commercially competitive, and geopolitically contested one — in which the United States, Qatar, Russia, China, and emerging African producers each hold partial and conditional leverage. The oversupply paradox — where abundance and scarcity coexist, and where a resource that trades in nominal surplus can see spot prices surge 300–400% within a single geopolitical event — will be its defining characteristic for the remainder of this decade. For industries dependent on advanced chips — from AI data centres to autonomous vehicles to defence systems — helium supply security has established itself as a strategic priority.

Key sources: USGS Mineral Commodity Summaries 2024; Intelligas Consulting — The 2024 & 2025 Worldwide Helium Market; Frontiers in Environmental Science (Cao et al., 2022); Tom's Hardware (March 2026); Reuters (March 2026); Yahoo Finance/South Korea chip supply analysis (March 2026); Helium One Global Tanzania (2025); Gazprom/TASS Amur (2023–2024); QatarEnergy/Air Liquide SPA (January 2026); Industrial Info Research (March 2026); EnkiAI Semiconductor Report (January 2026); Crux Investor helium price analysis (July 2025); Gasworld helium oversupply report (October 2025).

Communicator

Add Message