The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

Iran possesses approximately 208.6 billion barrels of proven crude oil reserves, representing roughly 12% of global reserves and ranking fourth worldwide. Current oil production stands at approximately 3.1-3.3 million bpd as of mid-2025, with exports estimated at 1.5-1.8 million bpd despite intensified U.S. sanctions enforcement. International Energy Agency projections suggest Iran could lead Middle Eastern production growth over the coming decade if sanctions ease, with potential to add 900,000-1.2 million bpd by 2030.

The refining sector's expansion must be understood within this context of constrained but potentially transformative production dynamics. Iran's strategy emphasizes maximizing value from available crude through downstream processing rather than relying solely on crude exports—an approach intensified by sanctions pressures that have complicated crude marketing while creating opportunities for refined product trade.

Perhaps no aspect of Iran's refining sector evolution has been more consequential than the forced march toward technological self-reliance. The 2018 cancellation of South Korea's Daelim Industrial's $2.08 billion contract to upgrade Isfahan refinery marked a watershed moment. Daelim's withdrawal, citing sanctions fears following Washington's nuclear deal exit, left Iran with incomplete engineering work and critical technology gaps.

Esfahan Refinery | Credit: Quds Online (June 15, 2021)

This episode catalyzed a fundamental reassessment of technology sourcing strategies. NIORDC and affiliated companies intensified collaborations with domestic engineering firms, universities, and research institutes. By 2023-2025, Iranian refineries reported substantial progress in equipment and catalyst localization:

Catalyst Production: Development of domestically-produced catalysts for FCC, hydrocracking, and reforming, including an RFCC catalyst containing 16 specialized components with 800°F heat resistance developed through collaboration between Shazand refinery engineers and Iranian startups.

Equipment Manufacturing: Production of over 17,000 refinery devices and spare parts domestically, yielding reported cost savings of approximately €80 million annually at individual refineries. This encompasses pumps, heat exchangers, instrumentation, and control systems previously sourced internationally.

International Partnerships: While self-reliance initiatives progressed, China's Sinopec emerged as Iran's most significant international technology partner, stepping into roles previously filled by Western firms. Sinopec's involvement at Abadan refinery—where it contracted for approximately $1 billion in upgrades including crude distillation expansion and hydrotreating units—illustrated Beijing's willingness to maintain energy sector engagement despite sanctions risks. Russia increasingly appears poised to fill roles as deepening Moscow-Tehran cooperation accelerates.

Current refining capacity of 2.4 million bpd across ten NIORDC-operated refineries represents substantial achievement, yet masks persistent execution challenges affecting major projects. NIORDC announced in August 2025 an ambitious plan to add 180,000 bpd of new refining capacity, with Isfahan refinery's RHU (Residue Hydrotreatment Unit) and RFCC (Residue Fluidized Catalytic Cracking) projects as centerpieces.

The RHU and RFCC units together represent approximately $1.2 billion in investment designed to convert heavy fuel oil into lighter, higher-value products. Originally targeted for completion in 2026, these projects have experienced delays related to equipment procurement challenges and financing constraints. The RHU will add approximately 12.5 million liters per day of gasoline and 1 million liters per day of diesel production. As of May 2025, NIORDC officials indicated completion now anticipated in the 2026-2027 timeframe.

Similarly, Abadan refinery underwent phased modernization raising capacity to approximately 390,000-400,000 bpd, with commissioning of a 42,000 bpd hydrocracker in 2024—the largest such unit in Iran. This achievement enabled production of Euro-5 specification fuels from heavy residues, addressing environmental standards and product quality objectives.

Aerial view of the Abadan refinery | Credit: OIEC Group

Isfahan Petrorefining Holding has announced plans for a "second site" 120,000 bpd refinery in Bandar Abbas, though this project remains in early development stages.

Iran will lead the Middle East region in conventional refining capacity additions through 2030, with potential to add 300,000-400,000 bpd if planned projects proceed on schedule.

The sanctions architecture affecting Iran's refining sector comprises technology export controls, financial sector isolation, petroleum export restrictions, and secondary sanctions threatening penalties against non-U.S. entities engaging with Iranian oil operations. Beyond economic measures, military threat dimensions add further complexity to sector planning. Following Iranian missile attacks in April and October 2024, speculation intensified regarding potential Israeli or U.S. strikes on energy infrastructure. Major refineries at Abadan, Bandar Abbas, Isfahan, and Tehran are large, stationary targets that would be difficult to defend, and temporary disruption of 500,000-1 million bpd could severely impact domestic fuel supply given Iran's limited excess capacity.

Iranian refineries have developed adaptive strategies to mitigate the combined impact of sanctions and security pressures, including barter and non-dollar transactions, front company networks for equipment procurement, technology reverse engineering efforts, and enhanced regional product trade with neighboring countries less sensitive to U.S. sanctions. Yet the U.S. administration has periodically intensified enforcement, most recently in September-October 2025 with sanctions targeting Chinese entities purchasing Iranian oil and financial networks supporting petroleum exports. These escalating measures aim to reduce Iranian oil revenues available for refinery investment, though historical evidence suggests Tehran prioritizes refining sector development even under severe fiscal constraints.

Iran's January 2024 accession to BRICS as a full member represents potentially transformative geopolitical repositioning with direct implications for refining sector development. The expanded BRICS bloc, now encompassing Brazil, Russia, India, China, South Africa, Iran, UAE, Egypt, and Ethiopia, collectively controls approximately 42% of global oil production and 36% of global refining capacity. For Iran, membership offers technology access channels, alternative financial architecture frameworks to circumvent SWIFT-dependent transactions, enhanced petroleum product export potential to BRICS member markets, and political capital in sanctions negotiations.

The deepening Russia-Iran strategic partnership, formalized through comprehensive cooperation treaty negotiations in October 2025, extends significantly into petroleum refining domains. Specific areas include engineering and construction services from Russian firms with extensive refining expertise, joint catalyst development initiatives, and sophisticated logistics arrangements for crude and product swaps.

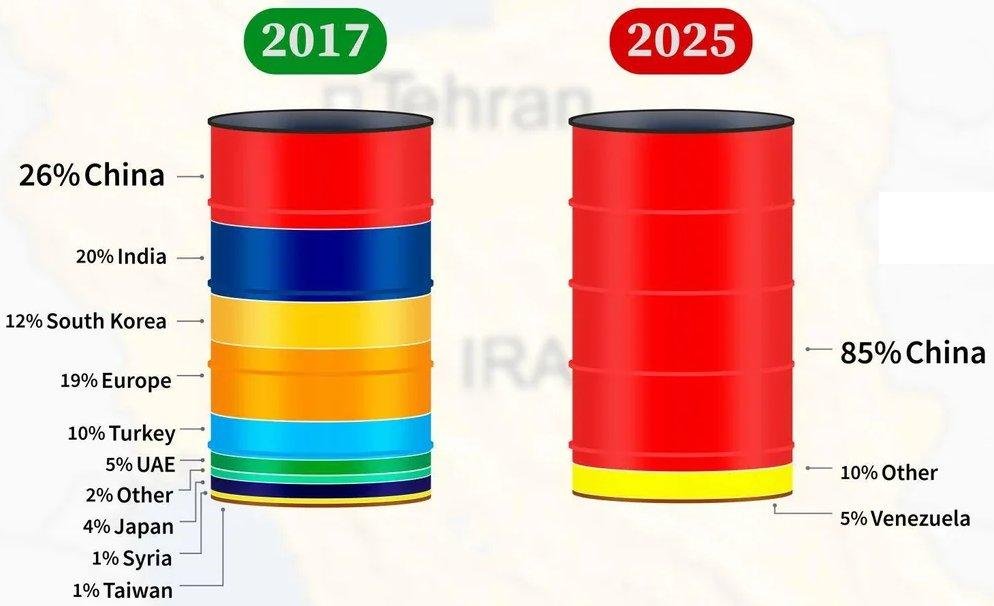

China's position as Iran's largest crude oil customer creates natural linkages to refining cooperation, though Beijing's approach remains calibrated to manage U.S. sanctions risks, as evidenced by the October 2025 Treasury actions against Sinopec.

Share of Iran's monthly oil exports: China buys almost all of Iranian crude oil

Credit: r/XGramatikInsights on Reddit, June 2025 | Data sources: Kpler and TankerTrackers.com

Improving environmental performance and achieving international fuel quality standards have emerged as priorities alongside capacity expansion. As of late 2025, NIORDC reported that approximately 70-75% of Iranian gasoline and diesel production met Euro-4 or Euro-5 specifications, up from less than 40% in 2020. Isfahan refinery commissioned a kerosene treatment unit in September 2025 producing Euro-5 kerosene, with 70%+ of total refinery output meeting European standards.

Nine refineries are currently implementing quality upgrade projects totaling several hundred million dollars in investment. Environmental compliance improvements serve dual purposes: addressing legitimate domestic public health concerns from vehicle emissions in cities like Tehran, and positioning Iranian refined products for export markets should sanctions ease and quality standards become competitive differentiators. Advanced water recycling systems, exemplified by Isfahan's 85% recovery rate, address Iran's severe water scarcity challenges while meeting international environmental standards.

Despite capacity expansion achievements, Iranian refineries face significant profitability pressures that complicate long-term financial sustainability. Domestic gasoline and diesel are sold at heavily subsidized prices far below international market levels and production costs, creating fiscal dependency on government budget transfers. Refineries receive no premium for producing higher-specification fuels, undermining economic justification for quality upgrade investments. Crude oil supplied at administered prices rather than market-linked rates creates artificial economics that may not reflect true opportunity costs. NIORDC has privately advocated for gradual subsidy rationalization and market-based pricing reforms, though political concerns regarding social reactions to fuel price increases have constrained policy implementation.

Current refining capacity of 2.4 million bpd significantly exceeds domestic demand for primary products, estimated at approximately 215-225 million liters daily. If sanctions ease substantially, Iran could potentially export 200,000-400,000 bpd of refined products to regional markets by 2030. However, competition from massive new refining capacity additions elsewhere in the Middle East and Asia may limit opportunities even without sanctions constraints.

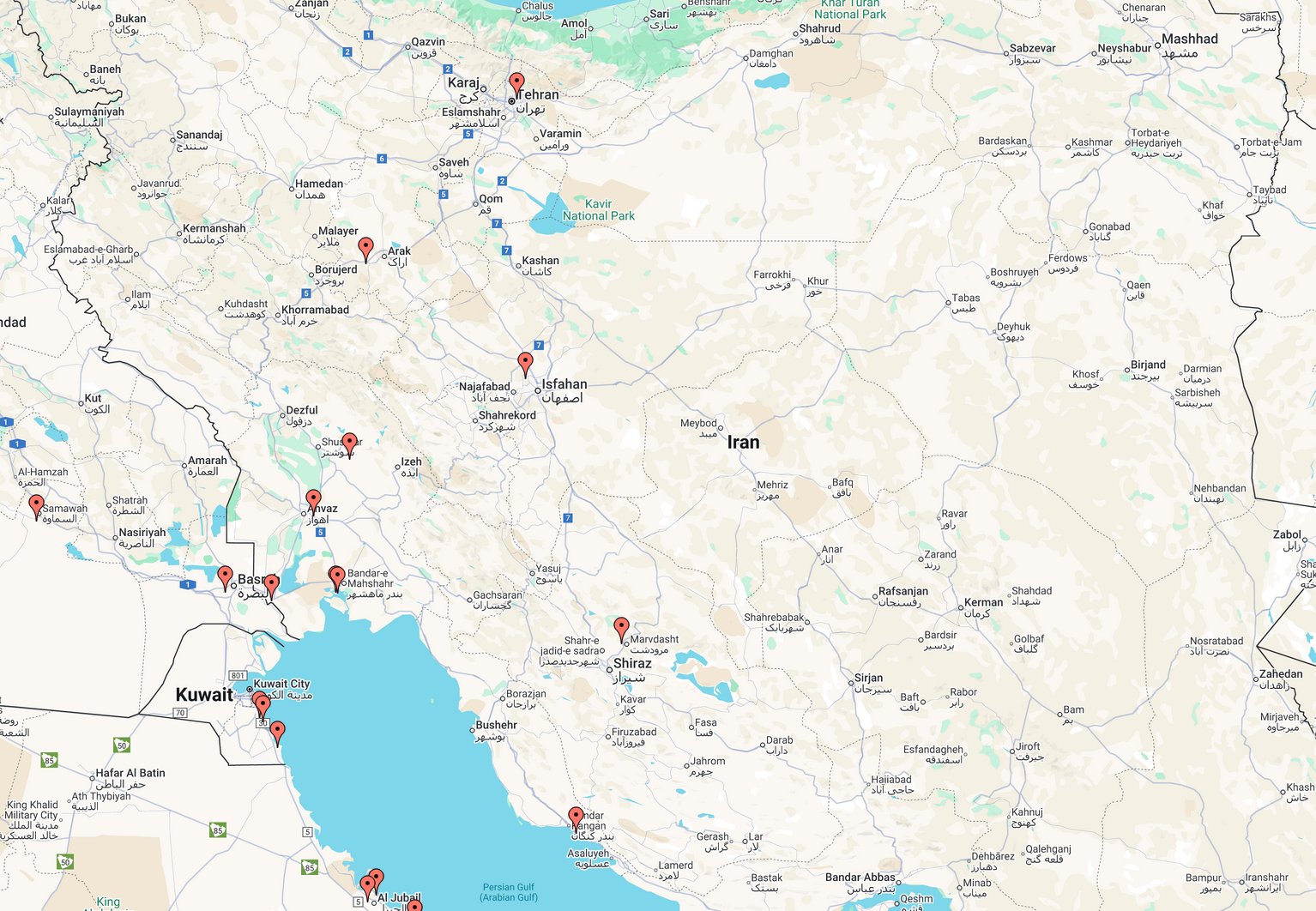

Map of Iranian refineries via refining module (Captured: Nov 1, 2025)

The most likely trajectory for Iran's refining sector through 2030 reflects a counterintuitive dynamic: sanctions have catalyzed rather than constrained sectoral development through forced technological self-reliance and deepening partnerships with Russia and China. This paradox defines Iran's energy strategy going forward.

Crude oil production will likely expand from current 3.1-3.3 million bpd to approximately 3.5-4.0 million bpd by 2030. This represents significant growth despite—and partially because of—sanctions pressures that have forced investment in upstream technologies, domestic equipment manufacturing, and alternative trading arrangements with BRICS partners. Refining capacity will expand to 2.8 million bpd through completion of delayed projects and intensified cooperation with Russian and Chinese firms now positioned as primary technology suppliers following Sinopec's October 2025 sanctions complications.

Refined product exports will expand to approximately 200,000-300,000 bpd through legitimized regional trade once sanctions architecture stabilizes or selectively eases, generating meaningful foreign exchange while demonstrating technological progress. This growth trajectory reflects Iran's capacity to transform external constraints into strategic opportunities through Eastern partnerships and technological innovation.

By 2030, Iran will possess 2.8 million bpd refining infrastructure with approximately 80-85% of production meeting Euro-4 or Euro-5 environmental standards, producing 3.5-4.0 million bpd of crude oil, and exporting both petroleum and refined products to BRICS and regional markets. This represents transformation not despite sanctions, but through deliberate leveraging of Eastern partnerships, domestic technological achievement, and strategic realignment away from Western-dependent development models. The refining sector emerges as an exemplar of how sustained external pressure, when met with institutional adaptation and alternative partnership frameworks, can paradoxically accelerate industrial modernization and diversification.

Sources: This analysis is inspired by research from over 50 sources including official Iranian government statements, international energy agency reports, industry publications, academic studies, and geopolitical risk assessments across English, Persian, Arabic, Russian, and Chinese language materials published between 2018-2025.

Communicator

Add Message