The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

... or why seemingly cheap feedstock (availability) is not a guarantor for success.

New investments continue to be announced in the Middle East about new petrochemicals projects or new integration projects with refineries. It is worthwhile to take a closer look at the results of two relatively young companies already operating, which are pillars of Saudi Aramco's strategy to build a diversified petrochemicals manufacturing base in the region: Petro Rabigh and Sadara.

Financially both companies struggled in the last 5 years (and before) to meet expectations of their shareholders.

Petro Rabigh Company (PRC), Refinery and Petrochemicals, was founded in 2005 by Saudi Aramco (SA) and Sumitomo and listed 2008 on the Saudi Stock Exchange (Tadawul). The 2024 Annual Report of PRC states the shareholding-% as:

Tadawul: 25%

Sumitomo: 37.5%

Saudi Aramco: 37.5%

SA announced in 2024 its intent to acquire 22.5% from Sumitomo, increasing their share in PRC to 60%.

PRC has been configured to benefit from feedstock availability and feedstock advantage in the region. Designed as a refinery with a processing capacity of 400,000 barrels per day (originally 325,000 bbls per day) and an ethane cracker, with a cracking capacity of 125 million standard cubic feed per day. (mmscfd)

The product slate of the refinery includes (all volumes in million tons per annum) Diesel 4.8, Fuel Oil 5.0, Gasoline 2.0, Jet Fuel 2.1 and also Naphtha 0.6.

The petrochemicals operation produces a wide range of Ethylene and Propylene derivatives and additionally aromatics like Paraxylene. Various expansion projects over the years and upcoming in 2025 have increased these assets capacities.

Sadara Chemical Company, established in 2011 as a joint venture between Dow Chemical Company (Dow) and SA. SA reports in their Annual Report for 2024 a shareholding of 65% of Sadara and Dow 35%. In August 2024 Dow announced that it signed a non-binding agreement to buy an additional 15% stake in Sadara to boost their interest to 50%.

Sadara was from the start an ambitious project, the "first-of-its-kind world’s largest ever complex built in a single phase", adding new value chains to Saudi Arabia's petrochemicals and derivatives industry.

This was to be achieved with the first mix-feed cracker of its kind in the region, processing 2 million tons of Naphtha and 1.1 million tons of Ethane in its original configuration, producing a wide range of Ethylene- and Propylene derivatives. (see flow-diagram) New technologies were introduced to the Kingdom to create an advanced configuration of the site. Details of the plants-technologies are available here.

Both ventures have been designed to benefit from Saudi Arabia's feedstock availability and a positive demand-outlook for their products, globally and in the Kingdom. SA has chosen with Sumitomo for PRC and Dow for Sadara two world-class partners for the project-phase and in the running of the operations. Both JV-partners also retain marketing rights for certain markets of the exported products.

Petro Rabigh and Sadara were envisioned to list on the Saudi Stock Exchange strengthening the public ownership of major industry players in the country. However only PRC made a public offering, providing interesting insights into the operations for analysts. Sadara's results are partially available in the their respective shareholder reporting and on the Tadawul website, as it signed up for a Sukuk-Bond.

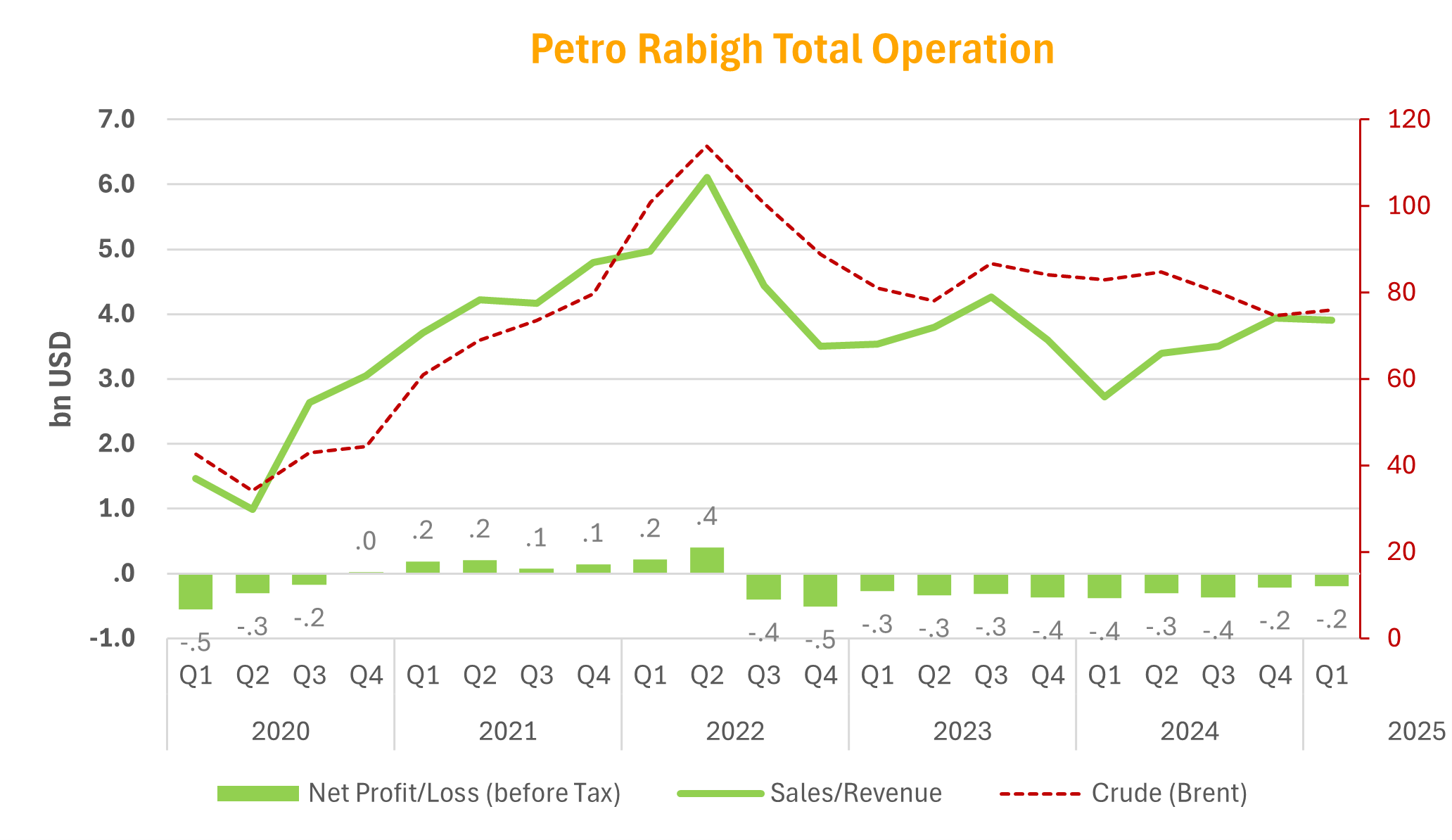

PRCs results were impacted over the years by technical reliability issues with numerous outages, impacting financial performance. The stock price development has been reflecting the problems over the years.

The results of the last 5 years have suffered during the Corona years, but high crude pricing and demand recovery only generated profits in 2021 and 2022.

Prior to 2020 PRCs results have been a mixed picture, with the petrochemicals compensating in many periods for losses generated in the refining section. The last 2 years have generated losses in both segments. Weak demand has resulted in low utilization rates for these years, which dropped from 76.7% in 2023 to 68.7% in 2024. The overall macro-economic factors will continue to impact PRC in 2025.

Source: PRC Annual and Quarterly Reports

The poor results and capital investments in expansion projects required additional shareholder funding via a rights issue in 2022 and influx of cash through the share acquisition of SA from Sumitomo. The mechanisms however still need to be determined. (PRC Annual Report 2024)

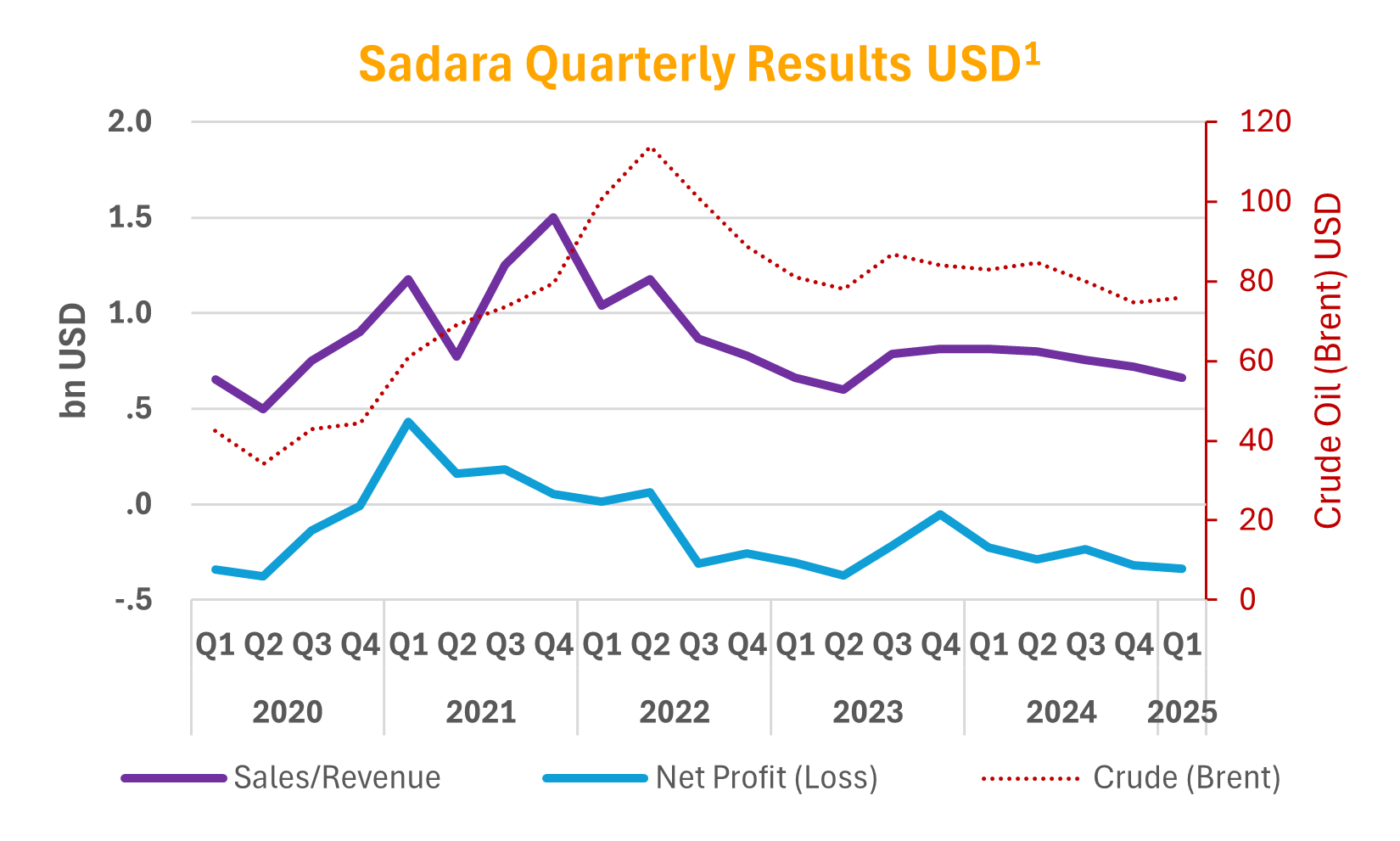

Over the timeline, Sadara's performance mirrors PRC's profitability cycle. The highly diversified product-slate does not protect the site enough from demand and price variations. This has become obvious from the start and the rather optimistic margin-projections could not be achieved and required major refinancing by the shareholders Dow and SA, and eventually with both companies writing off their investment in the company.

Unchanged economic parameters and a planned turnaround is impacting the results in Q1 2025.

Source: Saudi Stock Exchange Reporting

Both companies and shareholders now list multiple rationalisation and improvement projects to find a path back to profitability, but the economic environment needs to improve. Until then investors in the shareholding companies and in PRC can only trust (for good reason) the commitment of DOW and SA (and Sumitomo) to support the assets through the current climate of weak demand, new tariffs and increased regulations.

ppPLUS will continue to post updates on the quarterly performance of these ventures. Contact us, if you are interested in a full assessment of PRC and Sadara performance. (see below)

PRC and Sadara provide benchmarks for other investments in the region. Almost all of Saudi Aramco's refinery assets and refinery JVs are under strategic review for further petrochemicals expansion or already in the build phase, like the Amiral project at Satorp.

The United Arab Emirates are executing major expansions around the Ruwais refinery (Borouge and others) and also to a lesser extent OQ in Oman is expanding their petrochemicals portfolio.

Interesting learnings can be taken from both projects. They were designed with a clear strategic intent, convincing investors with obvious advantages and (too!) optimistic margin outlooks. A key factor for the project approvals will have been the feedstock advantage and its availability. But the present financial performance provides a clear picture, basing the decision on strategic ambition alone without a clear risk assessment is not enough to run such operations profitable.

High technological complexity, particular in the case of Sadara, together with an unfavourable market environment have put both companies into very serious liquidity situations. Red flags, such as "Refinancing", "Additional Funding" etc are recurring terms in the Annual Reports of the shareholders and other Analyst Reports.

We should assume that investors and analysts now take a more careful view on margin predictions and profitability analysis, however it is still easier to buy a story, when there is such a great strategic-fit and obvious advantages compared to other markets, like Europe or even the US. But PRC and Sadara clearly point out, that any outlook and risk assessment needs to consider a worst case scenario as a probable outcome.

Nowadays analysts can learn from the past in a different fashion than they used to. The cycles of the last 20 years, which has seen the financial crisis of 2008, drop in oil prices in 2014, Corona, tariffs etc must be assumed for any investment outlook.

The advantage now is, the data is available and if the business model implies an investment cannot sustain such a or multiple crisis it needs to be revisited again or even abandoned. Using challenging margin cycles the industry has experienced over the years will hold more usable facts for a financial outlook model than the conventional forward supply and demand data sets provided by many of the consulting services.

Petro Rabigh and Sadara in ppPLUS:

Communicator

Add Message